Warsh Hawks Outshine Mideast Truce. BoE Takes Stage Next.

8 min read

Share

Trump signed the MOU. Peace deal optimism cooled oil prices. Warsh's hawkish Fed stole the spotlight, lifting the dollar and reshaping FX sentiment. Sterling steadied ahead of today's BoE meeting, while the euro and Asian currencies adjusted to shifting rate expectations and fresh political uncertainty.

GBP: Sterling Waits for the BoE Verdict

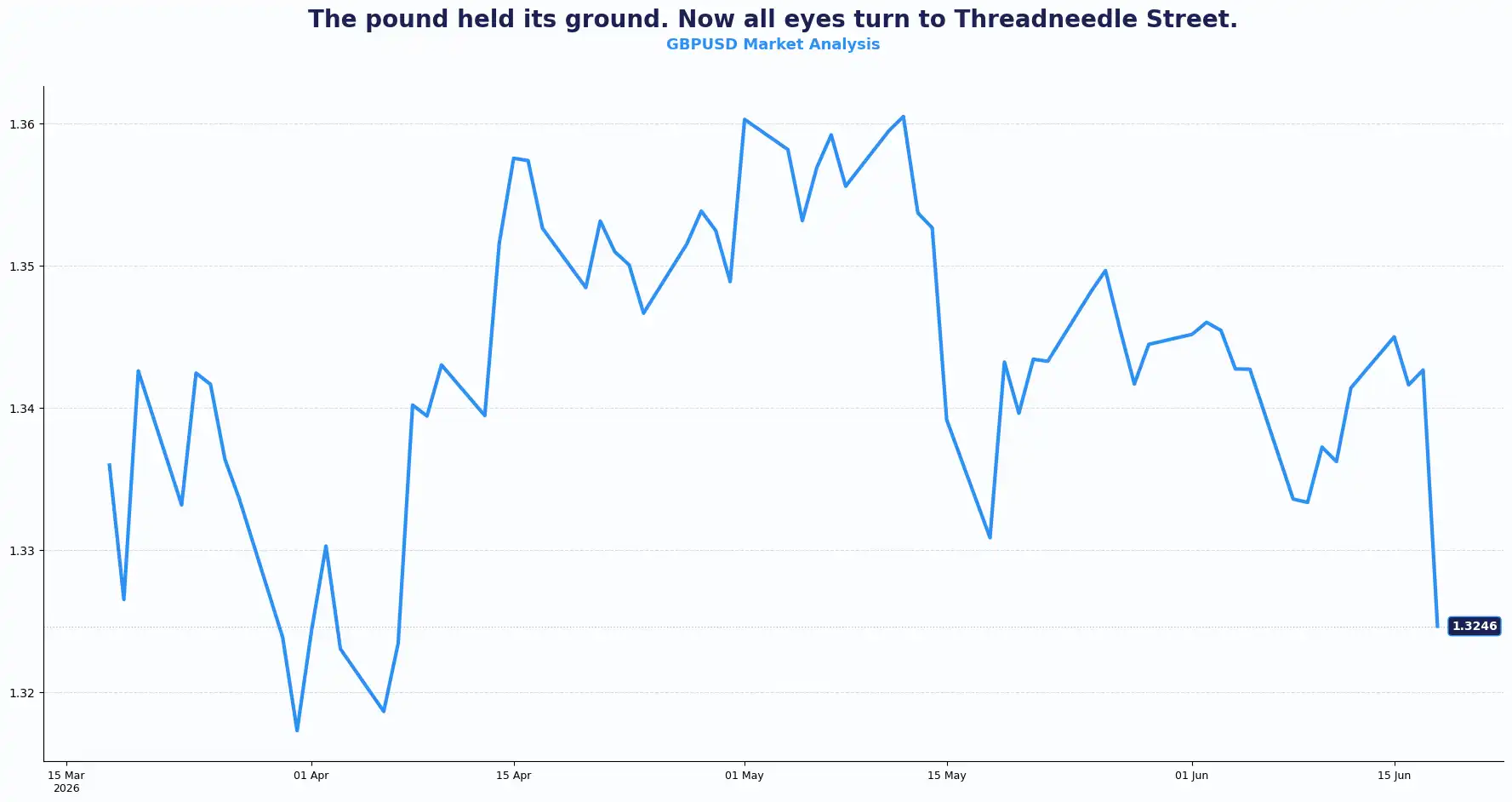

GBPUSD 1.3246

Sterling held near 1.3300 against the dollar despite softer UK inflation figures and mixed labour market dataIn the early European session before softening to 1.3240. Markets largely looked through the inflation release and shifted their attention to today's Bank of England (BoE) policy decision.

The GBP/USD pair retained its recent gains, though momentum faded as investors awaited guidance from policymakers.

UK CPI stayed at 2.8% in May, unchanged from April's 13-month low and below forecasts. The labour market picture arriving this morning gave mixed signals. The ILO unemployment rate ticked down to 4.9% in April, beating the 5.0% consensus. Employment change came in at 100K for the three months to April, below the prior 148K but above the 80K expected. Average earnings, both including and excluding bonuses, held steady at 4.4% and 3.4% respectively, neither accelerating nor retreating. The claimant count, however, jumped to 31,200 in May against a consensus of 25,800, signalling that the labour market is softening at the margins, even if the headline rate does not reflect it yet.

The BoE is expected to hold rates at 3.75%, in line with market consensus. What is of more emphasis today is the MPC votes and the split. Chief economist Huw Pill and potentially one other member of the Monetary Policy Committee (MPC) are expected to be possible dissenters pushing for a hike. One or two hawks voting against a hold is likely to shift market pricing. With the market currently pricing one BoE hike this year, any signal that the committee is growing more cautious could dislodge that expectation and weigh on sterling.

Brent Crude is sitting roughly 30% below its level since the last BoE meeting. The US-Iran peace agreement and the prospect of unimpeded shipping through the Strait of Hormuz could potentially pull energy inflation lower. That eases one of the BoE's key concerns about the second-round inflation outlook, which, in theory, softens the case for further tightening.

There is also a political subplot developing. Greater Manchester Mayor Andy Burnham is positioning himself to challenge Keir Starmer for Labour leadership. Burnham is seen as more interventionist on the economy than Starmer. The UK's fiscal headroom is already limited, and the memory of the 2022 Truss market episode has not faded. Historically, a leadership contest that introduces more fiscal uncertainty generally tends to attract a political risk premium into sterling pricing.

Tomorrow brings GfK consumer confidence for June and UK retail sales for May, two readings that might help sharpen the view on domestic demand before the next BoE meeting.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3350, 1.3400 and Support sits at 1.3250, 1.3200

EUR: The Euro Finds Its Floor Between Two Central Banks

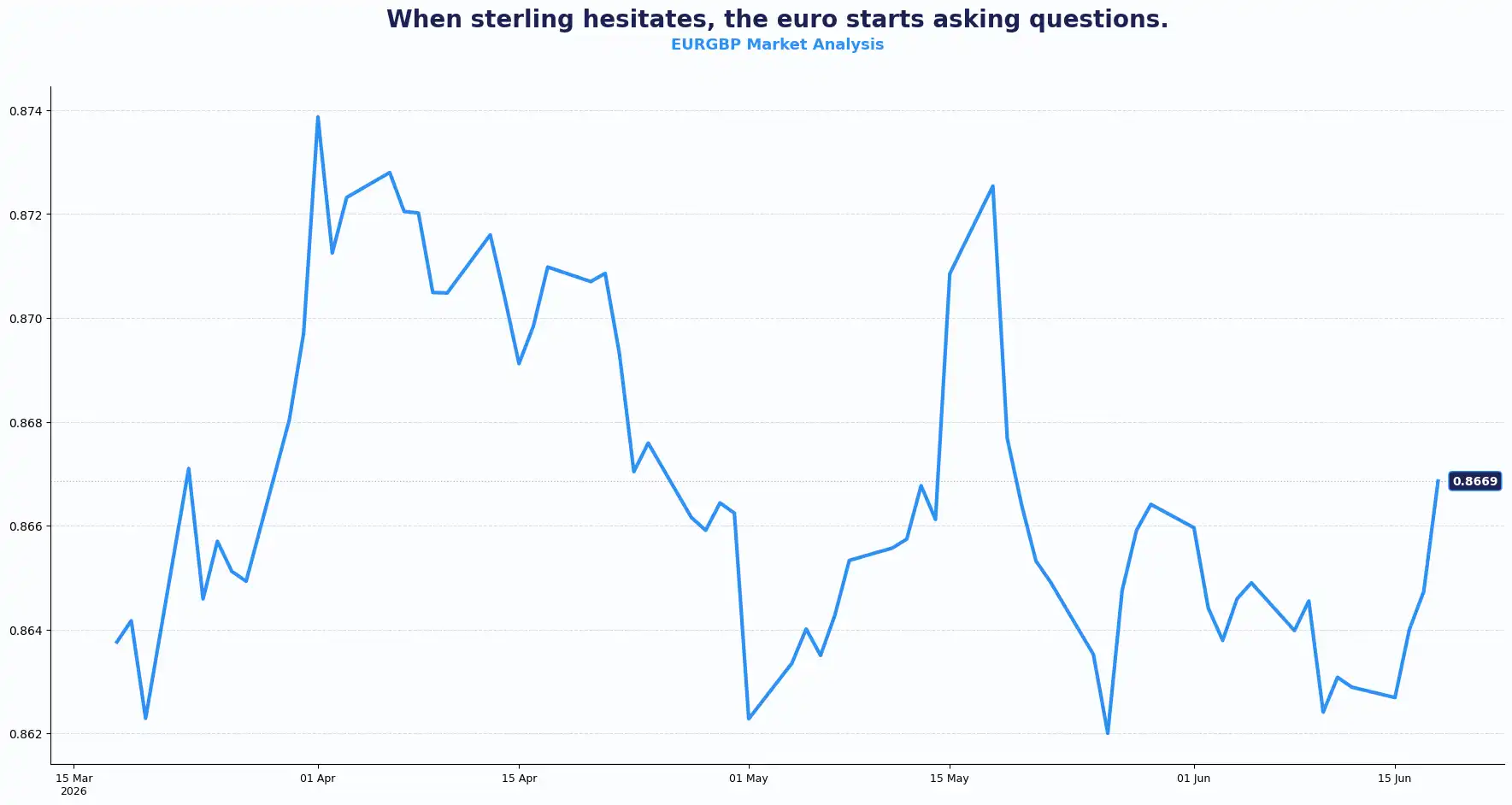

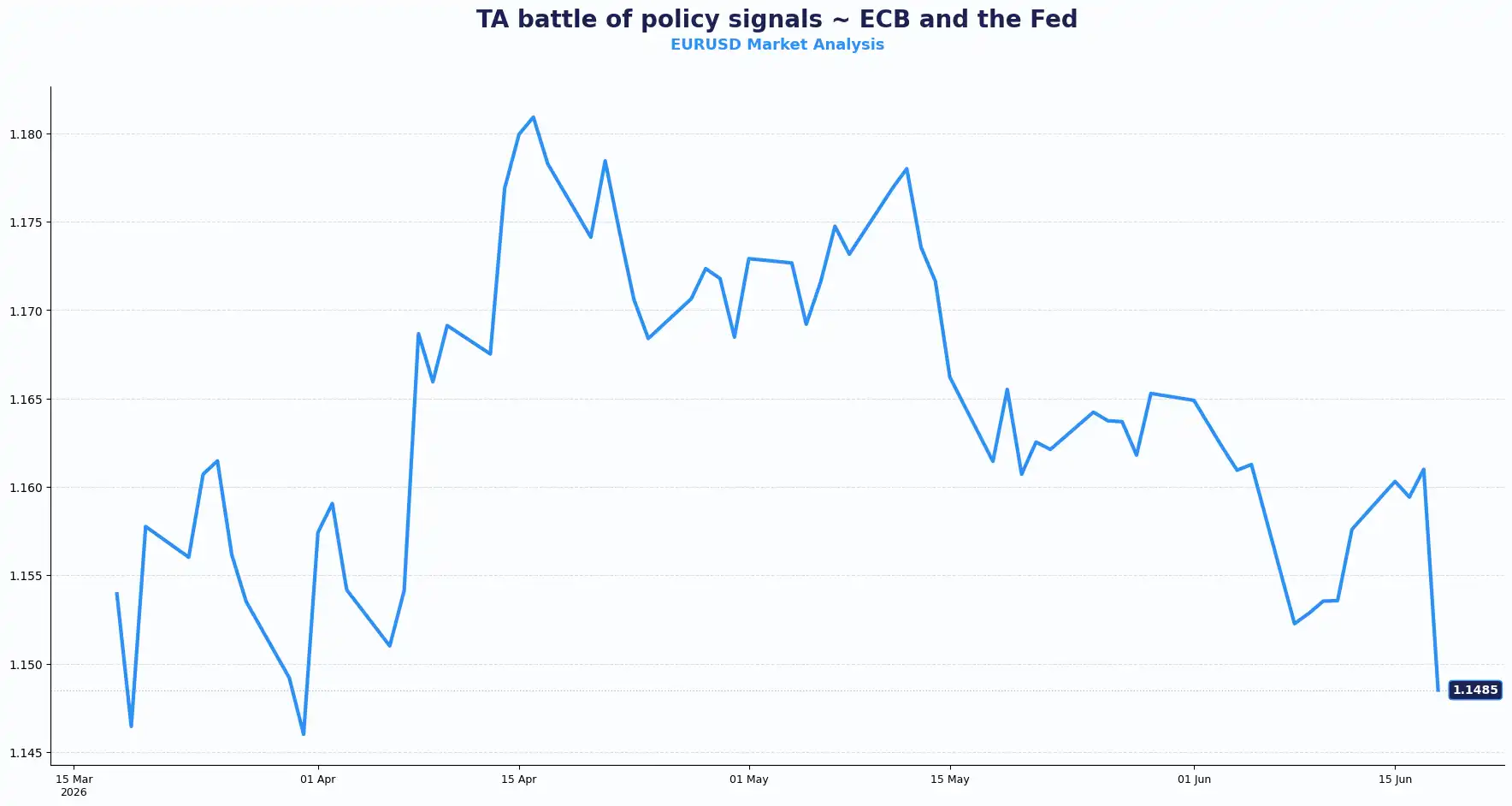

EURGBP 0.8669 | EURUSD 1.1485

The EUR/GBP pair steadied around 0.8660 in Thursday's early European session, with sterling's mixed employment data giving neither side clear momentum heading into the BoE announcement. The EUR/USD pair, meanwhile, pulled back from its intraday high and traded around 1.1518, about 0.5% softer on the session.

The euro's near-term trajectory sits between two competing forces. The European Central Bank’s (ECB) tone has leaned hawkish at recent meetings, and several governing council members speak today; those remarks could either reinforce or complicate the current market outlook on where Eurozone rates go next. On the other side, the Fed's shift has reasserted dollar demand and capped the EUR/USD pair’s upside.

The EUR/USD pair found a bid in Asian trade after touching lows around 1.1480, its weakest since late March. The pullback from those lows reflected a softening in the dollar after Trump signed the US-Iran MoU, knocking the geopolitical risk premium out of the dollar. The rebound brought the pair back to 1.1518, but the ceiling looks firm as markets bet on rate hikes in December at around 85% probability.

Tomorrow's German Producer Price Index (PPI) for May gives the next European data point. Consensus expects 0.7% MoM (against 1.2% prior) and 2.5% YoY (against 1.7% prior). A surprise on either side could shift ECB rate expectations and move the EUR/USD pair.

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8680, 0.8700 and Support sits at 0.8620, 0.8600

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1560, 1.1600 and Support sits at 1.1480, 1.1450

USD: Dollar Strength Persists Despite Geopolitical Relief

DXY 100.40

The US Dollar Index (DXY) surged toward the 100.40 mark on Wednesday and held near 100.26 in Thursday's session, anchoring the Greenback near a two-month high against major peers. This follows a highly anticipated debut press conference of the new Federal Reserve (Fed) Chair, Kevin Warsh, who delivered a hawkish hold.

The FOMC voted unanimously to hold the federal funds rate unchanged at 3.50%–3.75%. While the hold was priced in by markets, what came as a surprise was a notably firmer message than many had expected regarding the shift in language and the dot plot.

9 of the Fed's 19 policymakers now project at least one rate hike by the end of 2026. Warsh dropped the forward guidance framework, leaving no explicit signals about the path ahead. He told markets to price assets on their own reading of the data rather than reverse-engineering the dot plot. That is a significant shift in communication from the central bank. It appears that the Fed, under Warsh’s leadership, is keen on keeping its cards closer to its chest; borrowing a page from the Greenspan-era playbook of deliberate ambiguity.

The immediate market reaction looked something like this: Treasury yields rose, rate-hike bets for December climbed to 85% on CME FedWatch, and the dollar extended gains. Strong retail sales earlier in the week added fuel. The Fed's hawkish pivot overshadowed even the US-Iran peace deal progress, which, under other circumstances, historically would have weighed on the dollar by lifting the risk appetite and further softening energy prices.

Trump signed the US-Iran MOU on Wednesday, a geopolitical milestone that briefly lifted risk assets and sent oil and gold lower as the geopolitical premium faded. Bitcoin rallied to $66,315 on the news before sharply reversing to $64,339; the Fed's hawkish signal cut the recovery short. Oil prices eased after confirmation that the agreement aims to reopen the Strait of Hormuz to toll-free passage and restore Iranian oil flows. That takes commodity-linked inflation pressure down a notch, but the Fed's messaging signals the committee is not satisfied yet.

The Fed’s communication shift is significant to the currency markets. Investors now face a central bank that appears less willing to provide detailed forward guidance. That approach could increase uncertainty around future policy expectations and keep volatility elevated across major currency pairs.

Weekly US initial jobless claims data also arrive today and will be watched for any signs that labour market tightening is beginning to ease.

Yen, Aussie, Kiwi and the Asian Ripple

AUDUSD 0.7053 | NZDUSD 0.5806 | USDJPY 160.27 | GBPJPY 214.73 | USDCHF 0.7895 | USDCNY 6.7625

The USD/JPY pair held around 160.62, with the yen anchored in uncomfortable territory despite this week's Bank of Japan (BoJ) rate hike. Speculative short positions in the yen swelled to their highest since July 2024. Tokyo jawboned again, with Chief Cabinet Secretary Minoru Kihara stating that the government stands ready to respond to currency moves "at any time." That language is familiar. The current intervention has a higher threshold, but verbal pressure intensifies as the pair lingers near the 160 handle.

The GBP/JPY pair traded around 213.86, reflecting sterling's relative resilience on the cross.

The Aussie dollar climbed to 0.7037, and the New Zealand dollar gained to 0.5794. Both benefited from the Iran deal, reducing oil price pressure and stabilising equity sentiment, partly offsetting the drag from the Fed's hawkish turn. The USD/CHF pair weakened to near 0.7985 ahead of the Swiss National Bank (SNB) rate decision, with the SNB widely expected to hold at 0%.

China's onshore yuan weakened to a one-week low of 6.7690 against the dollar before recovering slightly to 6.7625. The PBOC fixed the midpoint at 6.8130. Two factors drove the move: broader dollar strength and a surprise drop in Chinese retail sales for May, the first contraction in more than three years. The PBOC authorised six major state banks to conduct offshore yuan transactions in Shanghai's free trade zone, signalling a preference for controlled yuan internationalisation rather than depreciation.

Asian currencies broadly consolidated in early trade. With the Fed now leaning more hawkish, the rate differential dynamics increase the relative attractiveness of dollar-denominated fixed-income assets, keeping pressure on Emerging Market (EM) and Asia-Pacific currencies.

Friday's Japan data slate includes the national CPI for May and the BoJ’s monetary policy meeting minutes. Those minutes could give insights into the committee's stance on the pace of normalisation and whether the yen's current weakness is influencing their thinking.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3246 | Sideways/cautious |

| EUR/USD | 1.1485 | Mild bearish bias |

| EUR/GBP | 0.8669 | Sideways |

| USD/JPY | 160.62 | Bullish (USD) |

| GBP/JPY | 213.86 | Sideways/bullish |

| AUD/USD | 0.7037 | Mildly bullish |

| NZD/USD | 0.5796 | Mildly bullish |

| USD/CHF | 0.7985 | Bearish (USD) |

| USD/CNY | 6.7625 | Bullish (USD) |

Market Lookahead

Thurs, 18 Jun

- BoE Monetary policy meeting, Interest Rate decision

- US weekly Initial Jobless Claims

Fri, 19 Jun

- UK’s GfK Consumer Confidence (June)

- UK Retail Sales (May)

- Germany Producer Price Index (May)

- Japan’s National CPI Inflation

- BoJ Meeting Minutes

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.