Super Thursday: BOE and ECB Close Out the Central Bank Week

8 min read

Share

Five central banks decided on rates this week. RBA hiked. Fed held with a hawkish tone. BoJ held. The BoE and ECB decide today with oil at $111 and stagflation risk on every desk. Super Thursday is live.

GBP: Tight Labour Markets Fuel a Hawkish BoE Pivot

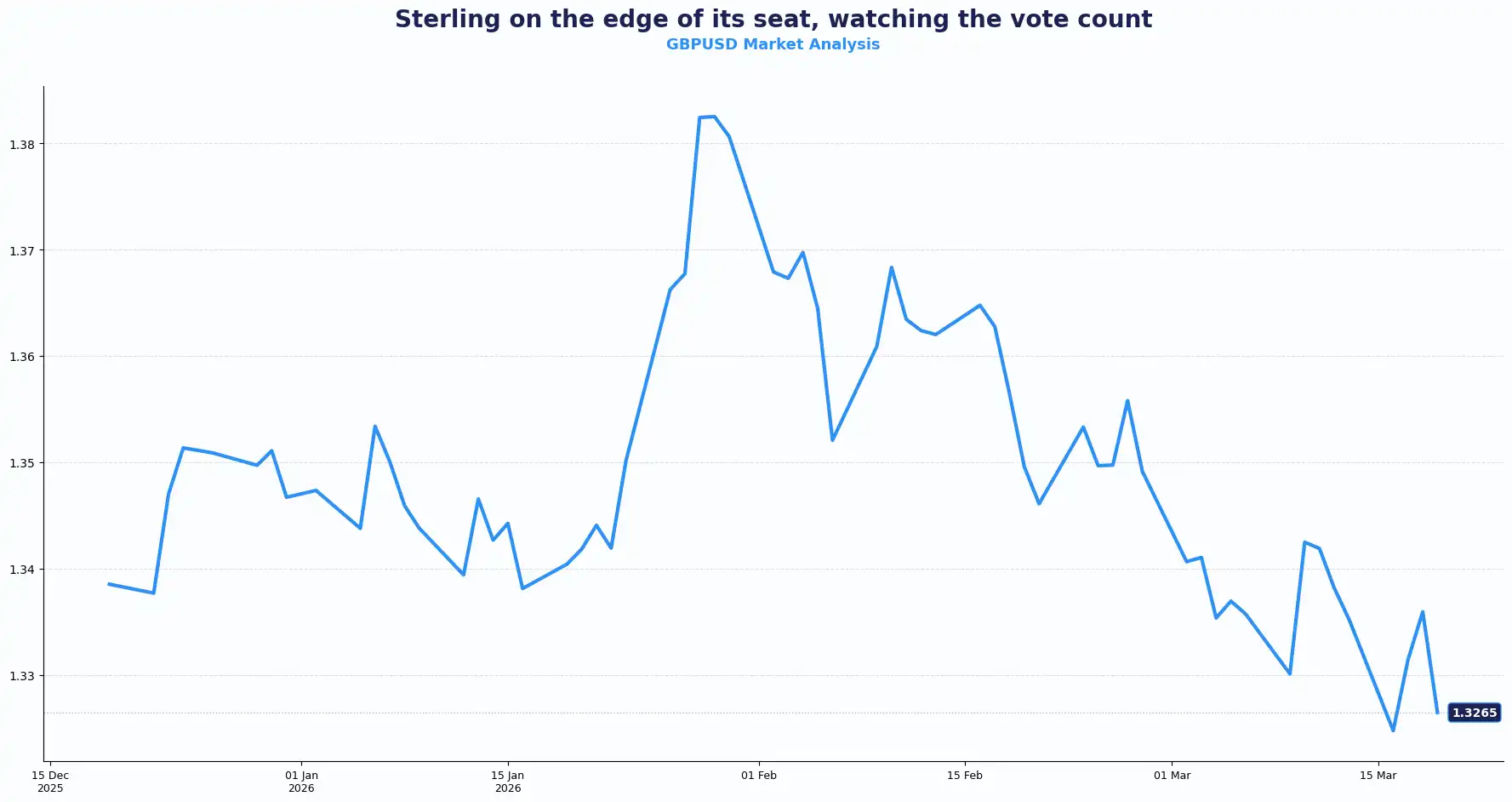

GBPUSD 1.3270 | EURGBP 0.8640

The UK labour market just delivered a masterclass in resilience, sending a clear message to the Bank of England (BoE) ahead of today’s high-stakes meeting. February’s Claimant Count Change arrived at 24.7K, tighter than the expected 25.8K. Meanwhile, the unemployment rate held firm at 5.2%.

The pound flexes its muscles as the UK jobs market refuses to cool.

Rising oil prices due to the escalating Iran conflict have pushed UK inflation expectations higher. This shift drastically reduces the chance of a March rate cut. Previously, traders priced in an 80% probability of a cut; now, the vote split holds the key. A 6–3 outcome signals a dovish tilt, while a 7–2 split aligns with the current hawkish consensus.

Wage growth is still stubborn, providing a critical anchor for the inflation outlook. Average earnings, including bonuses, hit 3.9%, while the ex-bonus figure was 3.8%. When paired with a massive 84K surge in employment change for the three months to January, it dismantles the narrative of a cooling economy. This data effectively anchors inflation expectations, making a "dovish" split at the BoE meeting today far less likely.

Policymakers now face a "stagflationary dilemma." Higher energy costs drive inflation up while simultaneously threatening to dampen economic growth. The BoE must balance these opposing forces. This makes an "extended pause" the likely path, rather than the easing many anticipated last month.

Tight labour markets create a structural floor for inflation. With 84,000 more people in work than last quarter, the BoE cannot easily justify a pivot toward lower rates. This "wage-push" pressure creates a policy divergence with lagging economies, directly supporting the pound’s valuation against the dollar and the euro.

Robust data often signals "higher for longer" interest rates, which keeps sterling expensive. For the BoE, the data doesn't change the outcome, but it does shift the texture of the conversation.

The Federal Reserve's (Fed) recent stance further complicates the GBP/USD pair’s trajectory. The Fed kept rates at 3.50%–3.75%, but Fed Chair Jerome Powell warned that the pace of disinflation is slower than desired. He explicitly noted that attacks on energy infrastructure will likely push prices higher. Policy divergence with the Fed continues to put pressure on GBP/USD. Expect tighter ranges until clearer signals emerge from the central bank tone.

Key technical levels for GBP/USD: Resistance at 1.3350 and Support at 1.3200

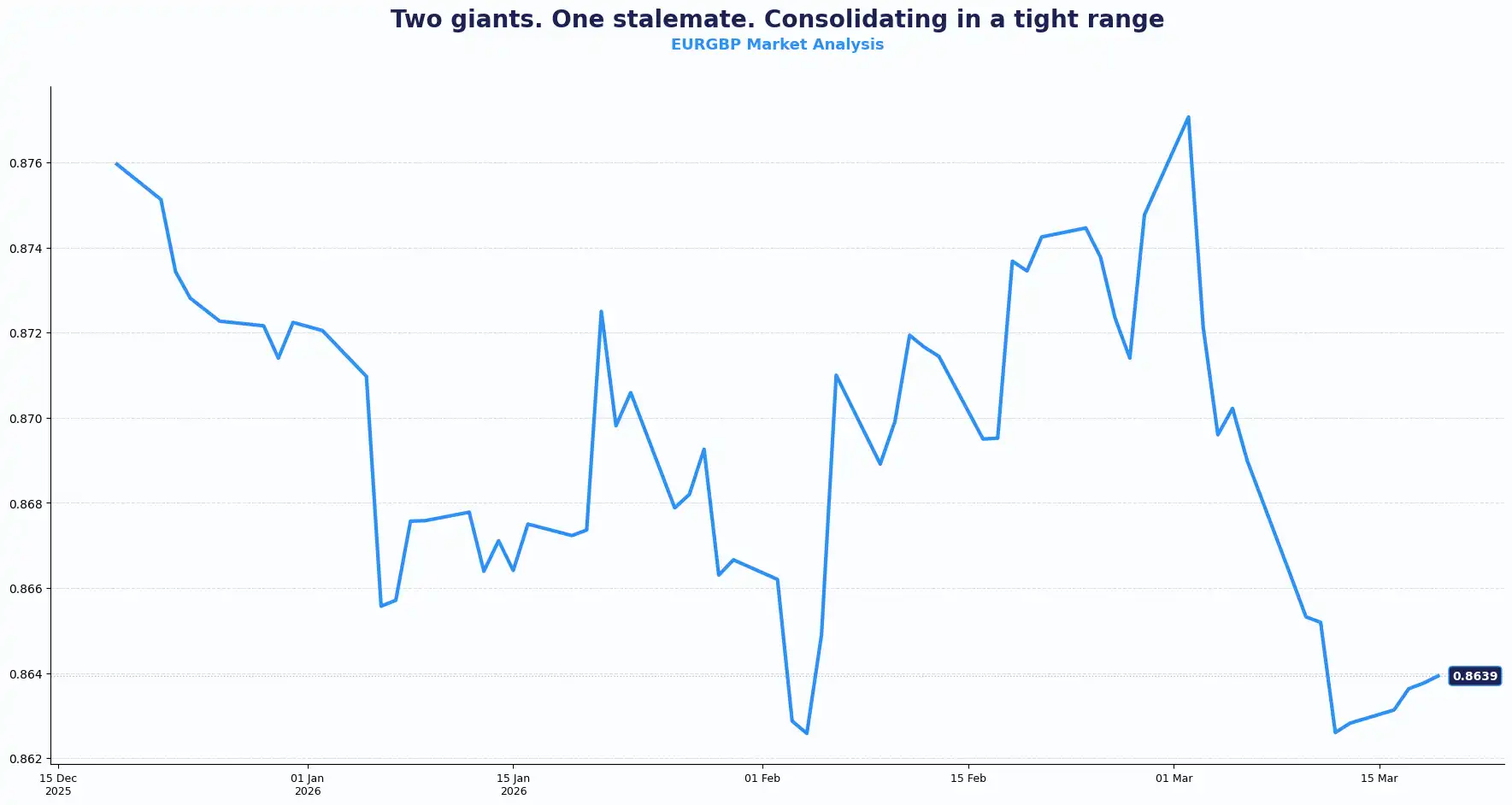

EUR/GBP consolidates near 0.8640; the cross stays range-bound until both the BoE and ECB press conferences conclude. Key technical levels for EUR/GBP: Resistance at 0.8700 and Support at 0.8600.

The BoE’s statement and Governor Bailey's press conference set further direction for sterling.

EUR: Lagarde Has the Floor And the Euro Is Listening

EURGBP 0.8640 | EURUSD 1.1470

The euro gains ground, trading near 1.1470 as the countdown to the European Central Bank (ECB) meeting begins. Investors expect the ECB to maintain the status quo, keeping the Deposit Facility at 2% and the Main Refinancing Operations Rate at 2.15% for the sixth consecutive meeting.

The single currency eyes the 1.15 handle amidst central bank divergence. Euro’s Aura: A hawkish glow with a shadow of energy risk.

The case for a hold is clear. Eurozone inflation has held close to the 2% target for a sustained period, and ECB officials have consistently pushed back against any policy adjustment. The energy shock, though, is shifting the calculus.

ECB President Christine Lagarde faces a dilemma. The consensus suggests she is likely to adopt a hawkish tone to prevent inflation expectations from de-anchoring.

Unlike the US, the Eurozone is more sensitive to energy imports, making the current Middle East conflict a direct threat to price stability. This forced hawkishness could support the euro against a basket of currencies in the short term. Divergence between the Fed and the ECB often creates rapid shifts in EUR/USD liquidity.

Traders have now fully priced a first-rate hike by September, with a 50% chance of a second move by year-end. The Fed's decision to hold and signal that cuts are off the table removes external pressure on the ECB to ease. EUR/USD momentum tilts upward as long as Lagarde leans hawkish, and the dollar does not catch a fresh bid. The upcoming press conference sets the stage for the pair's next leg.

Key technical levels for EUR/USD: Resistance at 1.1500 and Support at 1.1400

USD: Fed Holds Firm, Powell Talks Tough, Dollar Holds Bid

DXY 100.15

The US dollar index (DXY) hovers near four-month highs at 100.15. While the Fed held rates at 3.50%–3.75% at its March meeting, the new projections revealed the shift: lower growth, weaker employment, and higher inflation. PPI for February surged 0.7%, the largest monthly gain since last July; taking the annual rate to 3.4%, dwarfing the 0.3% rise economists forecasted.

The greenback finds its sanctuary in high yields and geopolitical risk.

Powell left no room for interpretation. Progress on inflation has stalled. Rate cuts will not follow until inflation moves closer to the target. He flagged rising oil prices from the Iran conflict as a near-term inflation driver but noted the Fed would look through the energy shock if core goods disinflation continues. His frustration at the pace of disinflation was explicit. Fed funds futures now price a December cut at barely better than a coin toss, pushing full easing expectations into 2027.

On the energy front, Brent Crude futures hit $111.42 a barrel. Attacks on regional energy facilities following the strike on Iran’s South Pars gas field fuel the dollar's sanctuary status, fuelling WTI crude to $96.65. Donald Trump's warnings about the South Pars field add a layer of geopolitical unpredictability, keeping investors anchored in the dollar. Even a 60-day Jones Act waiver to ease fuel deliveries failed to cool the market.

The Fed’s frustration means US rates stay "higher for longer." When energy prices act as a tax on global growth, the US economy’s relative resilience attracts capital flows. This reinforces the dollar's dominance. Factory orders rose 0.1% in February, matching expectations and confirming that the engine is still humming despite the heat.

A surging dollar increases the cost of USD-denominated imports and complicates global supply chain pricing. Treasury yields are rising, and the DXY's path of least resistance is higher unless inflation data softens or geopolitical conditions shift.

Antipodean Stress and the Yen’s Threshold

USDJPY 159.69 | GBPJPY 211.93 | AUDUSD 0.7041 | NZDUSD 0.5819

The BoJ voted 8-1 to keep rates unchanged. The yen is under pressure just below 160, the level traders widely expect to trigger intervention. Japanese Finance Minister Satsuki Katayama said authorities are on heightened alert, with recent yen weakness driven partly by speculative flows. Governor Ueda's press conference is now the focal point. How he frames the inflation-versus-growth trade-off sets the yen's direction. Most analysts still expect a BoJ rate hike at the April meeting.

GBP/JPY trades near 211.85, pulling back from the Asian session high of 212.35. Safe-haven yen demand is capping the cross ahead of the BoE decision.

AUD/USD edged to 0.7053 after Aussie unemployment ticked up to 4.3% in February, slightly above estimates. The RBA flagged the Middle East conflict as a material risk to the domestic economy. The data is mixed: not weak enough to signal a cut, not strong enough to lift the Aussie.

NZD/USD trades at 0.5819 after New Zealand GDP rose 0.2% in Q4, below both analyst and central bank forecasts. The data confirms some economic momentum before the oil shock hit. The miss, though, leaves the NZD exposed if energy prices stay elevated.

Global Macro: The Stagflation Tightrope Is Back

The same tightrope policymakers walked in 2022 when Russia's invasion of Ukraine sent commodities surging; is back. Risk-off dominates: equities are sliding, rate cut expectations are being pushed out, and the dollar is in demand. Oil is firmly above $100 a barrel; natural gas is up more than 6%.

Rate hikes cannot increase oil supply. They can only suppress demand, and that carries a growth cost. This is no longer a geopolitical headline story. It is a macro one. The question has shifted from "when do central banks cut?" to "how much damage does this energy shock do?"

Current Rate Table:

| Pair | Level | Short-term Trend Bias |

|---|---|---|

| GBP/USD | 1.3271 | Range-bound, downside capped |

| EUR/USD | 1.1469 | Gradual upside, resistance near 1.1500 |

| EUR/GBP | 0.8642 | Consolidation |

| USD/JPY | 159.69 | Uptrend, intervention risk near 160 |

| GBP/JPY | 211.93 | Sideways to lower |

| AUD/USD | 0.7041 | Mild recovery |

| NZD/USD | 0.5819 | Weak bias |

(rates as at the time of writing)

Market Lookahead

Thu, 19 Mar

- GBP - BOE Rate Decision

- EUR - ECB Rate Decision - Deposit facility rate

- USD - US Initial Jobless Claims

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.