Sterling Tests the Ceiling as War Clouds Linger

9 min read

Share

UK Core CPI beats the call at 3.2%. BoE April meeting now turns live. UK and Eurozone PMIs disappoint. The dollar holds at DXY 99.4 amid Iran ceasefire noise. G10 volatility is climbing as headlines steer price action across the board.

GBP: Sterling Eyes 1.34 as UK CPI Puts the BoE on the Spot

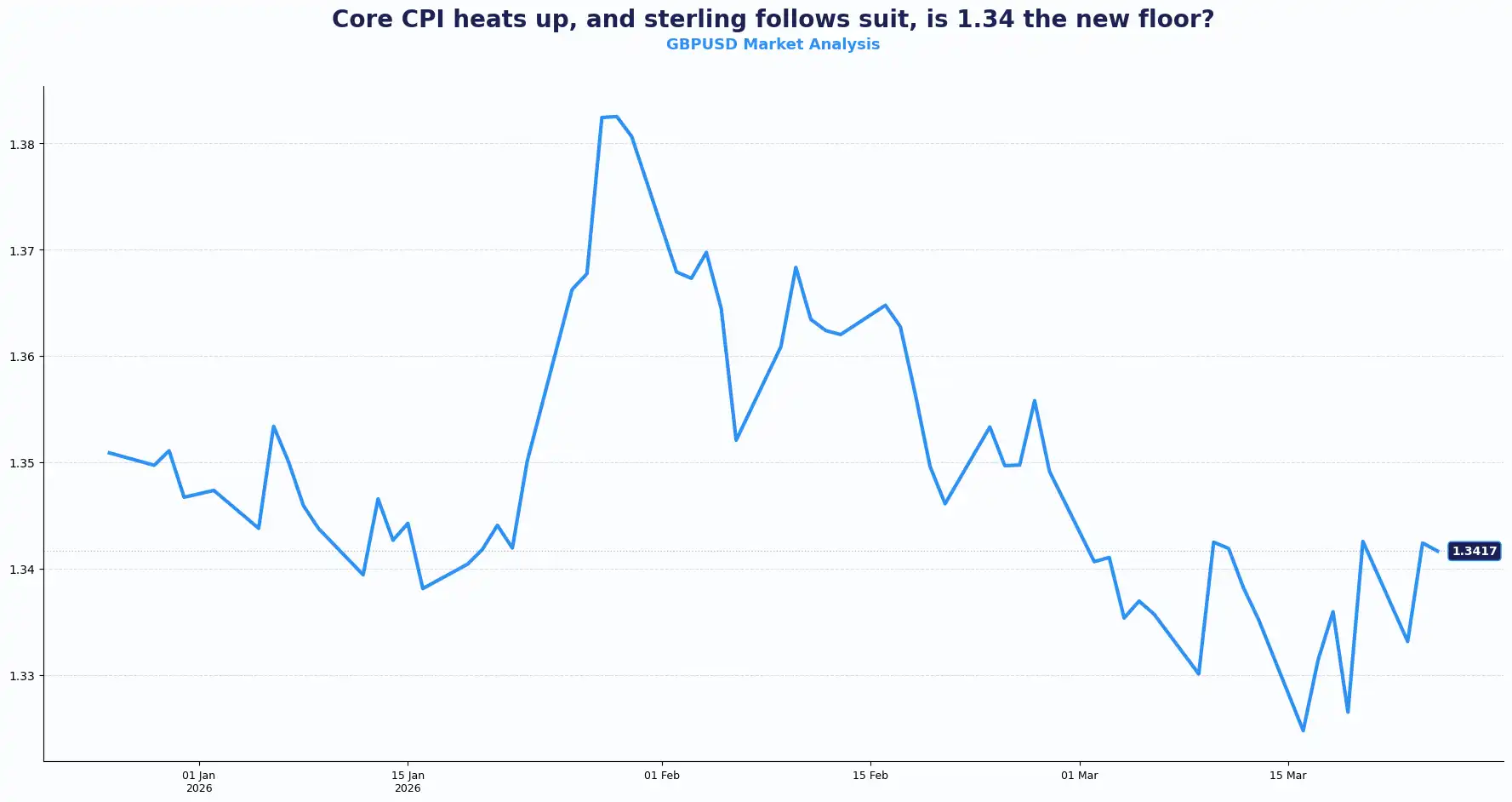

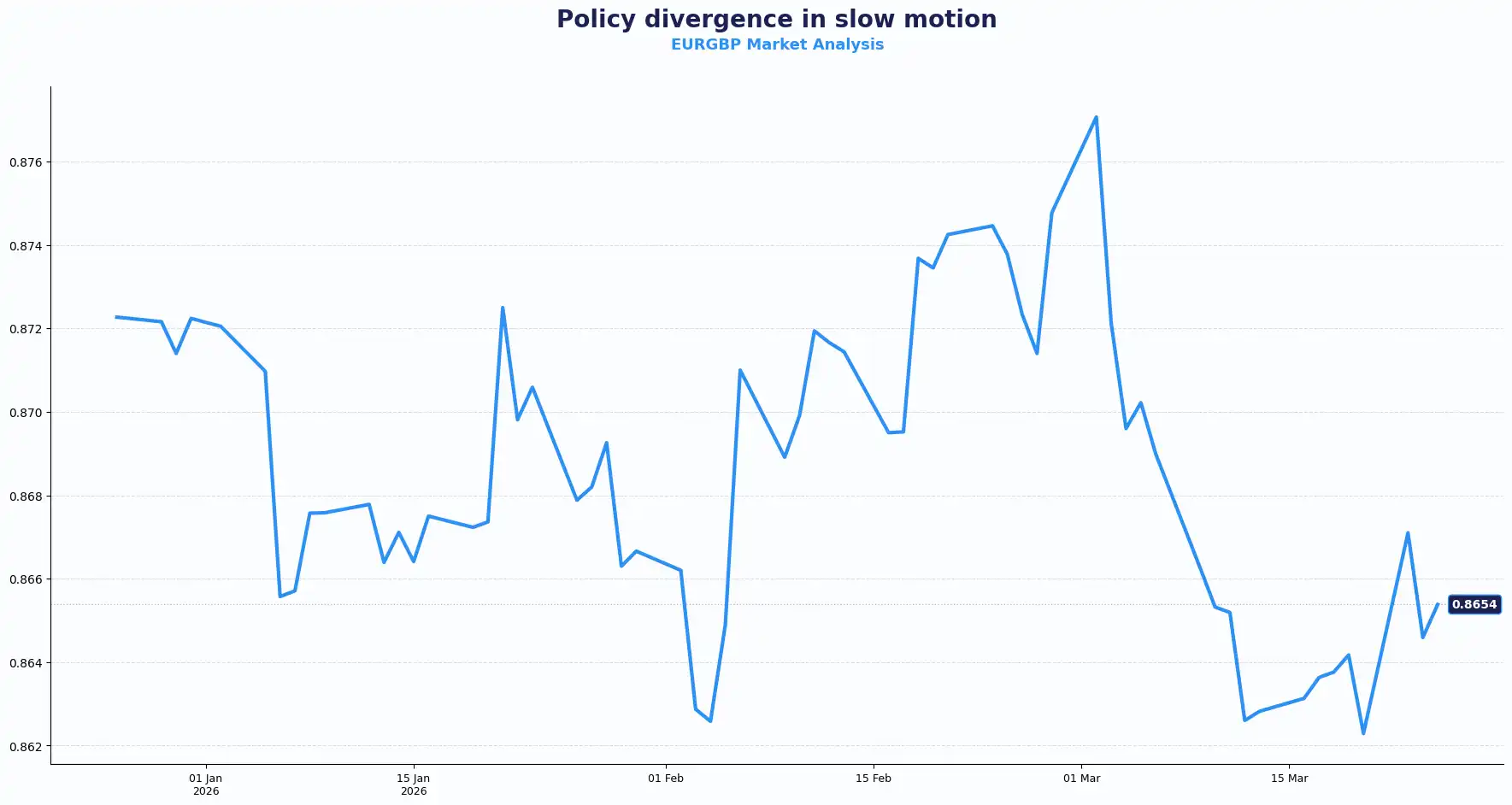

GBPUSD: 1.3428 | EURGBP: 0.8662

The British pound gripped to $1.3428 today as February inflation data landed with a thud. Headline CPI arrived at 3.0% on the year. This matches the January print and confirms that price pressures refuse to cool.

More importantly, the monthly figure jumped by 0.4%, erasing the previous month's contraction. Core CPI, the metric the Bank of England (BoE) watches with predatory focus, accelerated to 3.2%. At 3.2%, it clears the MPC's own projection range ceiling. That is not comfortable for a committee that just voted 9-0 to hold and flagged mounting upside risks to price stability. Sterling now tests the heavy 1.3400 ceiling with renewed vigour. Traders clearly see a central bank with its back against the wall.

UK Inflation Data, February 2026 Released Wednesday 25 March

| Indicator | Actual | Consensus | Prior |

|---|---|---|---|

| CPI (MoM, Feb) | 0.4% | 0.4% | -0.5% |

| CPI (YoY, Feb) | 3.0% | 3.0% | 3.0% |

| Core CPI (YoY, Feb) ▲ BEAT | 3.2% | 3.1% | 3.1% |

| Retail Price Index (MoM, Feb) | 0.4% | 0.5% | -0.5% |

| Retail Price Index (YoY, Feb) | 3.6% | 3.7% | 3.8% |

| PPI Input (MoM, Feb) | 0.8% | 0.5% | 0.3% |

| PPI Input (YoY, Feb) | 0.5% | 0.4% | -0.4% |

| PPI Output (MoM, Feb) | -0.5% | 0.2% | 0% |

| PPI Output (YoY, Feb) | 1.7% | 2.6% | 2.5% |

Source: ONS. Indicative at time of writing.

This data removes any excuse for a dovish pivot. While headline numbers stayed flat on an annual basis, the core beat of 3.2% signals that internal price pressures have nested in the UK economy. Input Producer Price Index (PPI) surged 0.8% on the month. This suggests that the cost of raw materials and energy continues to bleed into the supply chain. Although Output PPI fell 0.5% in February, the 1.7% year-over-year gain keeps pressure on margins.

The BoE now faces a stark reality. Governor Andrew Bailey previously warned about petrol prices and second-round effects. Today’s numbers prove those fears have merit. The Retail Price Index (RPI) hit 3.6% annually, which keeps the cost of living high and wage demands sharp. Huw Pill, the Chief Economist, recently noted that the fog of uncertainty cannot justify inaction. This inflation print clears that fog. The 9-0 hawkish hold from the last meeting now looks like a precursor to a definitive hike on 30 April. Policy makers must prioritise price stability over growth concerns as energy shocks from the Middle East filter through the data. Implied rates already priced roughly 67 basis points of tightening for the year. This print does nothing to argue that back.

UK PMIs added a note of caution. The S&P Global Composite PMI dropped to 51 in March from 53.7. Services fell to 51.2. Cost pressures from energy and supply disruption are intensifying. Inflation is sticky. Growth is softening. That is the needle the BoE is threading right now.

EUR/GBP held flat at 0.8662 ahead of the data. Dual PMI weakness across the Eurozone and the UK had kept the cross range-bound throughout the session. The core CPI beat shifts the risk balance toward mild sterling outperformance on the cross.

Implied volatility in sterling options rose ahead of the CPI release. A core beat of this kind has historically been associated with the repricing of near-term BoE rate expectations and shifts in sterling positioning. GBP/USD holds near 1.3379 with the 1.3428 resistance back in focus. However, a sustained break above 1.3420 could see the pound chase the 1.3500 handle if retail sales on Friday show any signs of resilience. On EUR/GBP, 0.8620 comes back into view.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3428 and Support sits at 1.3200, 1.3010

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700 and Support sits at 0.8600

EUR: Growth Slows, Stagflation Risk Builds

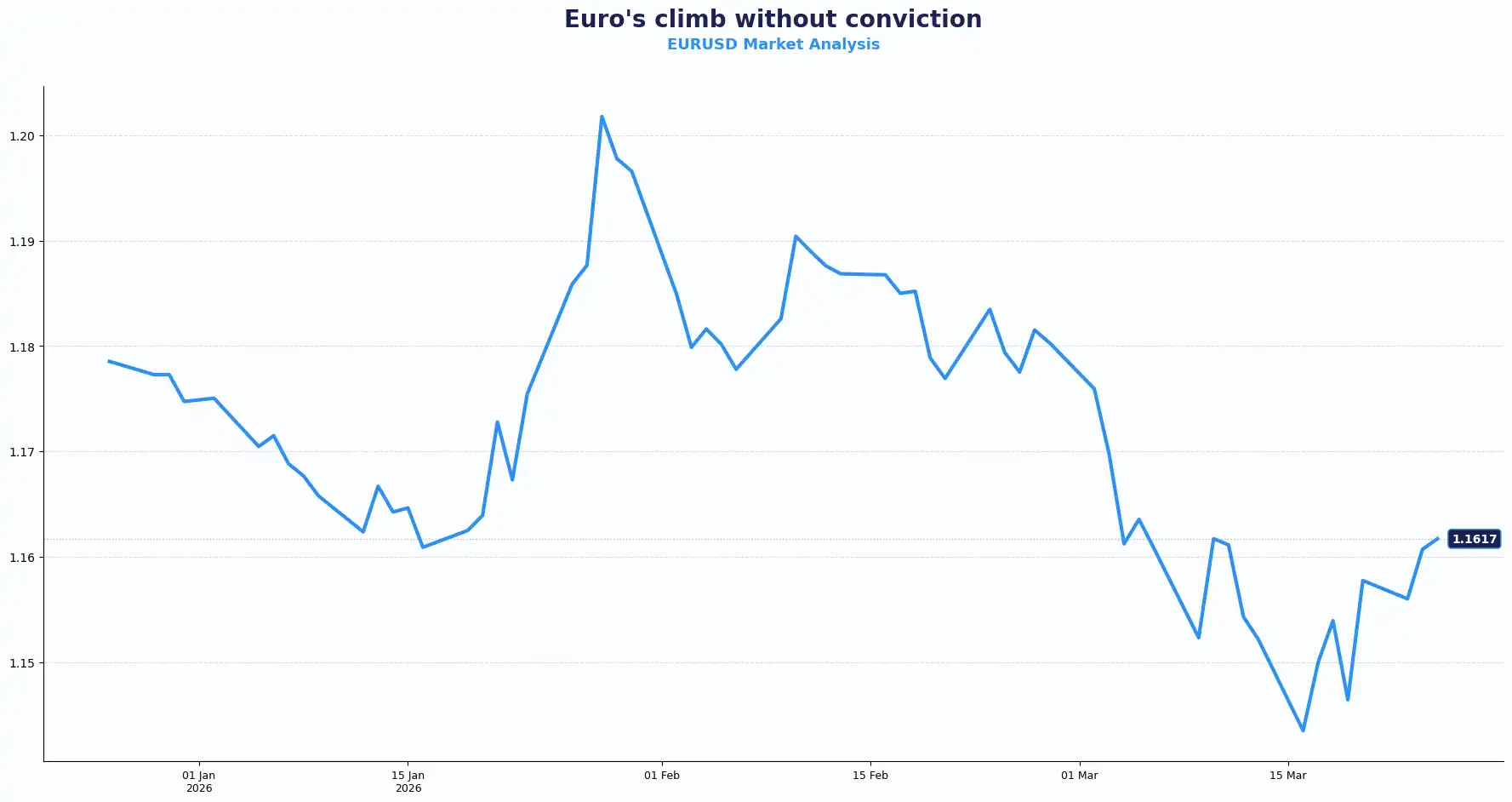

EURGBP: 0.8662 | EURUSD: 1.1590

The euro edged toward 1.1600 against the dollar today. This move happened despite a clear lack of momentum in the regional economy. Private sector growth in the bloc nearly stalled this month. Delivery times soared and costs rose. The currency pair holds its ground purely on the back of dollar hesitation rather than domestic strength.

The HCOB Composite PMI fell to 50.5 in March. This reading fell below consensus. A sharp slowdown in the services sector to 50.1 dragged the overall figure down. While manufacturing showed a slight recovery to 51.4, it cannot carry the entire economy. The Middle East conflict is driving energy prices higher and disrupting the Continent's fragile supply chains.

We see a classic stagflationary setup. Firms' costs rise at their fastest pace in three years, yet growth stays elusive. This creates a nightmare for the European Central Bank (ECB). This leaves the ECB with a difficult choice to fight inflation without crushing what little growth survives. The divergence between a hawkish UK and a stumbling Eurozone keeps the pressure on EURGBP. Until the energy picture clarifies, the euro is likely to struggle to find any meaningful upside beyond technical bounces.

EUR/USD edged higher through the session. Most other pairs showed limited movement. Participants held back from chasing moves driven by headlines that can reverse sharply. Tehran denied that direct talks with Washington took place. Iran's official news agency quoted an armed forces spokesperson who said the U.S. is "negotiating with itself." Conviction is thin, and the cross knows it.

Resistance at 1.1600 for EURUSD looks formidable. Economic damage in the bloc deepens by the day. This suggests that any euro strength lacks a structural foundation. The absence of clarity on ceasefire progress is a constraint on extended exposure. Near-term implied volatility across EUR crosses has risen in line with geopolitical uncertainty.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1600, 1.1650 and Support sits at 1.1450

USD: The Dollar Pivot: Diplomacy and Deficits

DXY: 99.39

The dollar index (DXY) sits near 99.39. Mixed signals from Washington keep the greenback steady. US President Trump recently claimed progress in negotiating an end to the war with Iran. He cited an unnamed Iranian concession "worth a tremendous amount of money." Tehran countered this, calling the claims "fake news." Oil prices fell, and stocks rose on the headlines, but the dollar refused to retreat significantly.

Against this backdrop, U.S. business activity slowed to an 11-month low in March. Higher energy and input costs feed into this slowdown. The S&P Global Composite PMI fell to 51.4 from 51.9. Services came in at 51.1. Manufacturing stood out at 52.4, beating the 51.0 consensus and rising from 51.6 in February. The Federal Reserve (Fed) now faces a dilemma. Inflation stays above the 2% target, but the manufacturing sector shows signs of wear.

In response to these pressures, Fed Governor Michael Barr said rates may need to hold steady "for some time" before further cuts are warranted. He cited inflation above the 2% target and geopolitical risk as key constraints. Fed funds futures now price a 30.2% chance of a 25-basis-point hike at the December meeting, up sharply from 8.2% the prior day. Bond trading stabilised after a volatile week. Yields on the 10-year Treasury dropped to 4.35% as participants weighed the chance of a ceasefire. Higher oil prices added to expectations of rising inflationary pressure and the prospect of tighter policy ahead.

The dollar finds support because it acts as the ultimate haven during geopolitical chaos. If Trump’s 15-point peace plan fails, the flight to the dollar will likely accelerate.

The dollar reacts to headlines, but inflation drives the trend. The "higher for longer" narrative supports the greenback on every dip. If negotiations fail, expect the dollar to assert its dominance once more.

Pacific Pressure: Energy Shocks and Intervention

AUDUSD: 0.6969 | NZDUSD: 0.5808 | USDJPY: 158.97 | GBPJPY: 212.80

AUD/USD held below 0.7000 after Australia's February CPI came in at 3.7% YoY, below the 3.8% consensus. NZD/USD traded in a 0.5800-0.5830 range. In Tokyo, the yen steadied near 158.97. This follows a volatile start to the week, during which officials teased potential intervention. USD/JPY held near 159.00. GBP/JPY traded at 212.80.

Energy-importing economies in Asia face a lasting hit. The Australian XJO, South Korea's KOSPI, and Japan's Nikkei 225 all gained around 2% on optimism over a ceasefire. Brent crude fell 5% on those same headlines but is still up 35% since the war began, with the barrel near $100.

Japanese officials signalled readiness to act to defend the currency amid oil’s impact on the yen. The yen drew support from that commentary. Reports also indicated Japan's Finance Ministry is exploring intervention in crude oil futures to blunt the yen's exposure to energy prices.

South Korea's National Pension Service said it will work to raise its long-term strategic hedging ratio to help stabilise the won. Typically sought as safe-haven assets, Gold recovered some ground but is on course for its largest monthly fall since 2008, while Bitcoin and Ethereum both gained. Stress signals are surfacing in private credit, an area that geopolitical noise has overshadowed, but one that participants are now tracking.

The "carry trade" faces a new era of volatility. With the BoJ potentially stepping in and the RBA turning softer, the cross-rate landscape is shifting.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3379 | Range-bound, mild upside |

| EUR/USD | 1.1590 | Cautious upside, low conviction |

| EUR/GBP | 0.8662 | Flat, rangebound |

| USD/JPY | 158.97 | Uptrend |

| AUD/USD | 0.6969 | Bearish below 0.7000 |

| NZD/USD | 0.5808 | Weak, range bound |

| GBP/JPY | 212.08 | Bullish bias |

(as at the time of writing)

Market Lookahead

Wed, 25 Mar

- ECB President Lagarde speaks

- Germany IFO Business Climate (Mar)

- US Import/Export Prices (Feb)

Thu, 26 Mar

- US Initial Jobless Claims

Fri, 27 Mar

- UK Retail Sales

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.