Six G10 Banks Hold. One Hikes. The Hawks Are Circling.

7 min read

Share

This week the BoE, ECB, Fed, BoC, BoJ and SNB all stood pat. The RBA hiked. The Middle East energy shock has shattered the low-volatility assumptions of 2025 and repriced the rate outlook across the G10. Oil is still near highs at $106, pushing most central banks toward a hawkish stance; the Fed the notable exception, holding its ‘wait-and-see position’ as Powell called for more time to assess the conflict's true economic impact. Sterling and the euro gain ground. The dollar slips from its peak.

GBP: Sterling Firms up as the Old Lady Finds Its Teeth

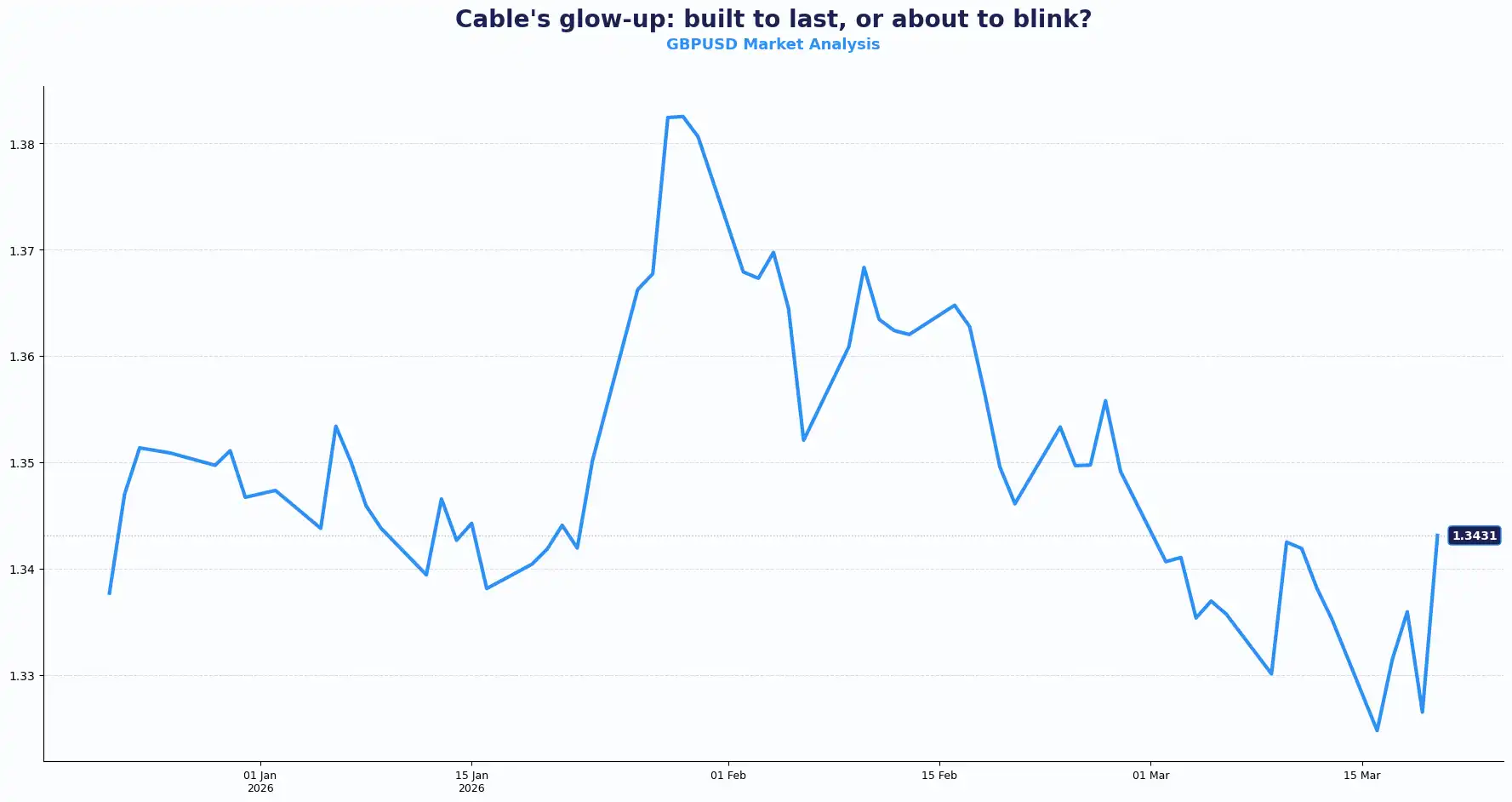

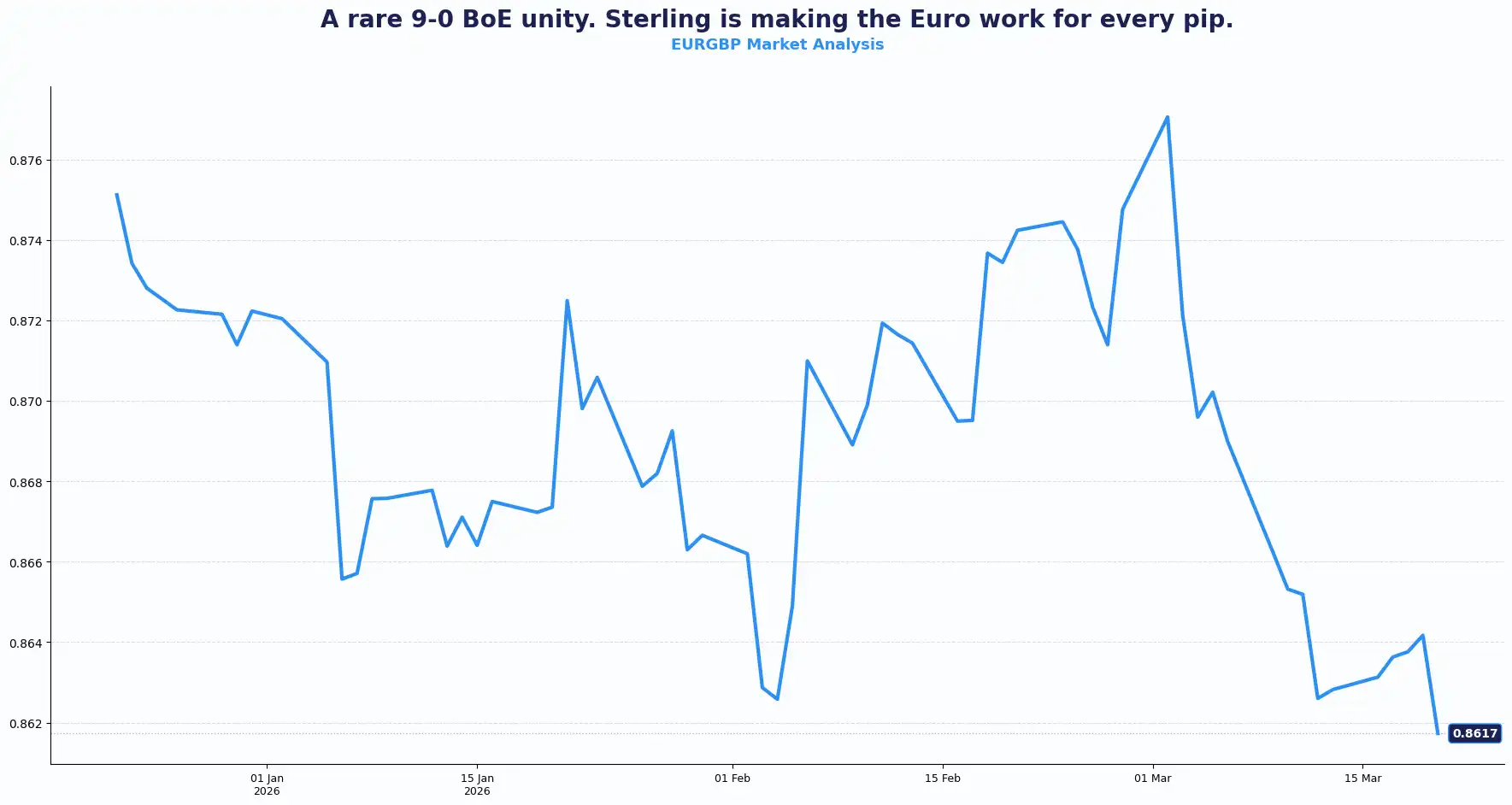

GBPUSD 1.3436 | EURGBP 0.8621

The Bank of England held the Bank Rate at 3.75% yesterday, matching forecasts but sparking a sharp rally in the pound. GBPUSD surged to 1.3436 as the Monetary Policy Committee (MPC) delivered a unanimous 9-0 vote to hold, a massive shift from February’s 5-4 split. This unity caught the market off guard, triggering a rout in short-dated gilts. Swap markets moved instantly. Investors now price in 80 basis points of hikes by year-end as the "wait-and-see" era ends. EURGBP sits near 0.8621 as the pound outpaces the euro.

The UK's structural position as a net energy importer makes its inflation profile far more "sticky" than that of the US. While the Federal Reserve (Fed) chooses to stay non-committal, the BoE has pivoted toward a restrictive stance to combat rising energy costs. The Monetary Policy Committee (MPC) now expects CPI to be 3.0–3.5% over the next two quarters, up from its April forecast of 2.0%.

The UK enters this shock at a period of below-potential growth (Q1 GDP estimated at just 0.1%-0.2%), forcing the BoE into a hawkish corner to prevent inflation from becoming entrenched. Even a short-lived confrontation, the BoE minutes noted, will delay the restoration of energy production. That distinguishes it from 2022, when demand ran hot and the policy calculus was more straightforward.

The Committee kept its options open in both directions. Rate rises are on the table if the shock deepens and embeds inflation expectations. Governor Andrew Bailey declined to pre-commit to any policy direction in his post-meeting pool interview. The meeting minutes tone, though, read hawkish. Wage growth data for the three months to January showed the slowest pace since late 2020. In ordinary conditions, that would reassure the Committee, but the Iran conflict has overtaken that signal.

This transition from internal division to a united hawkish front provides Sterling with a significant tactical cushion. While the "stagflation" mix of high energy costs and low growth pose a risk, the BoE’s commitment to its 2% target has influenced market behaviour. Any further spike in oil prices would tighten financial conditions and weigh on growth.

Key technical levels for GBP/USD: Resistance at 1.3450, 1.3500 and Support at 1.3300, 1.3200

Key technical levels for EUR/GBP: Resistance at 0.8700 and Support at 0.8580, 0.8500

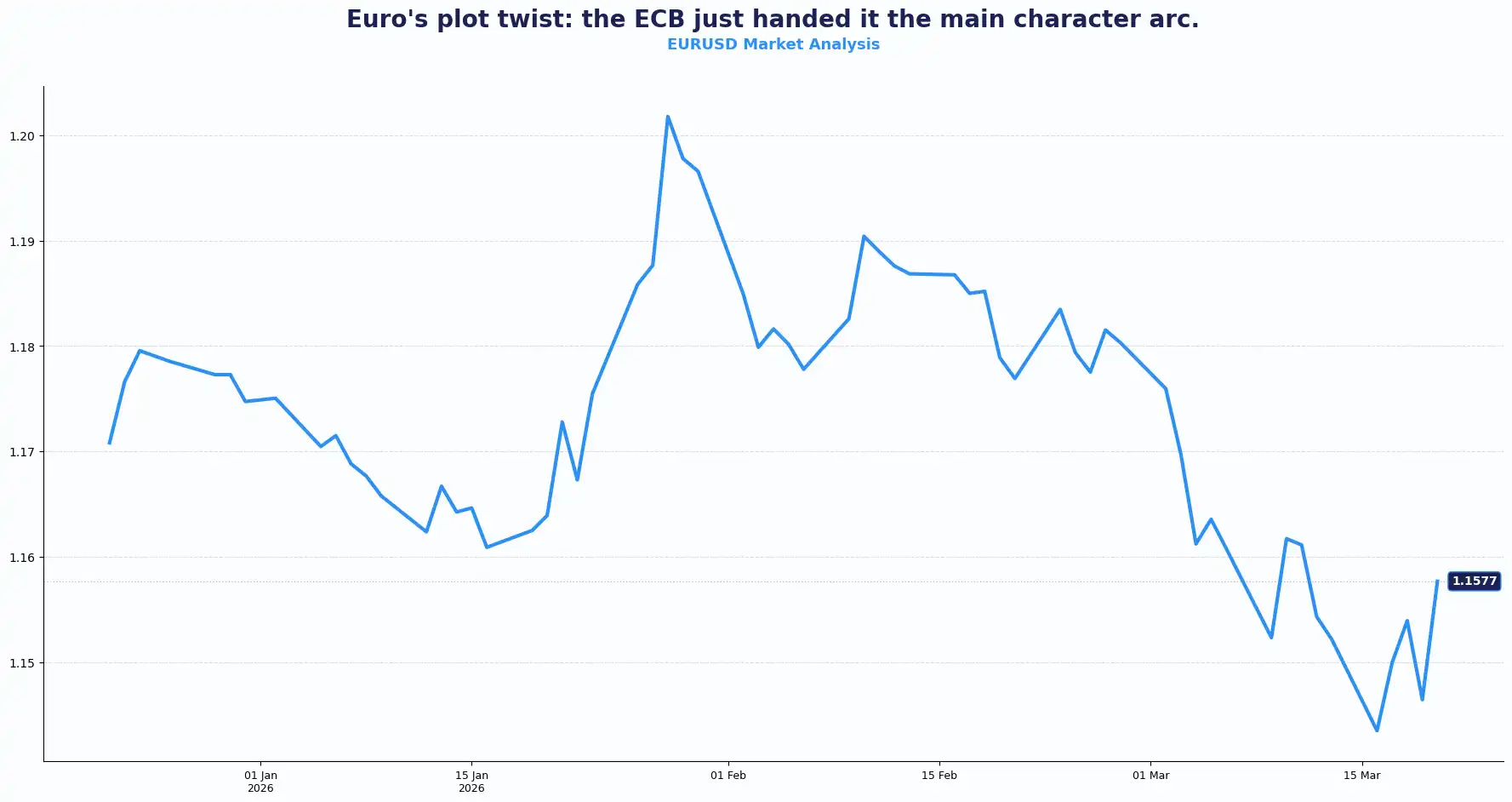

EUR: ECB Holds. A June Hike Enters the Frame.

EURGBP 0.8621 | EURUSD 1.1558

The euro gained 1.2% this week, trading at $1.1558 following yesterday’s European Central Bank (ECB) meeting. Although ECB President Christine Lagarde kept rates on hold, her rhetoric moved the dial. Investors have abandoned expectations for a long pause, now pricing in a potential "insurance hike" as early as June. The market is effectively betting that policymakers, wary of being "late" as they were in 2021, will pull the trigger sooner this time.

The ECB revised its 2026 GDP growth down to 0.9% (from 1.2%) while raising its inflation forecasts up to 2.6% (from 1.9%). This creates a clear divergence: while the Fed signals a pause, the ECB is preparing to act against secondary energy effects. This "hawkish gap" is currently the primary driver for the euro, providing structural support even as energy prices stay elevated.

The ECB’s shift has led to a tactical rotation back into the euro. With the 2026–2028 inflation outlook revised upward, the currency is no longer just a "funding" play. Traders are closely monitoring upcoming inflation data, as any further upside will likely accelerate the timeline for the first hike. The Governing Council retained its data-dependent framing, leaving the rate path live in either direction. The next projections round will test whether June delivers a hike or another pause.

Key technical levels for EUR/USD: Resistance at 1.1600, 1.1700 and Support at 1.1450, 1.1350

Dollar retreats as the Rate Gap Narrows

DXY 99.46

The dollar index held at 99.46, on course for a 1% weekly decline, its largest drop since late January. For weeks, the dollar was the undisputed king of safe havens, but the hawkish pivot from other G10 central banks has halted its momentum. As Brent Crude trades near $106, the narrative has shifted from "US Exceptionalism" to a global race to contain energy-led inflation.

Before the US-Israeli operation against Iran in late February, investors had priced two Fed cuts in 2025. One cut now looks distant. Yet the ECB, the Bank of England, the Bank of Japan, and others repriced faster and further. Rate differentials, the engine of dollar strength through 2024, have compressed, and the dollar has followed.

Fed Jerome Powell held to a wait-and-see position. The Fed's stance: the true economic impact of the conflict needs time to surface. That patience stands in direct contrast to the ECB's tightening signal and supplies the euro with a structural tailwind against the dollar.

Oil prices are up nearly 50% since the conflict began. It is the macro variable that reshaped the week. The US is an energy exporter. It absorbs an oil price shock differently from the UK or the eurozone, which is why the Fed can afford to be patient when others cannot.

Despite the dip, the dollar's downside is likely limited by ongoing geopolitical tension. However, the immediate trend has cooled as other currencies regain their "yield teeth." That tension between repricing of the tension rate and safe-haven flows defines the dollar's near-term path.

Global Ripples: The East Prepares for Change

The yen traded near 158 per dollar after the Bank of Japan held rates and maintained its tightening bias. April is now live for a potential hike. Investors who had bet on yen weakness were caught offside, and the reversal was sharp.

The Swiss franc weakened after the Swiss National Bank held rates and flagged readiness to intervene against recent franc strength. The safe-haven surge had extended beyond the SNB's comfort level.

The Australian dollar consolidated near 0.7100. The Reserve Bank of Australia hiked earlier in the week, the sole G10 central bank to do so, and gave the Aussie a firm footing entering the weekend. The New Zealand dollar traded at 0.5882, softer on the crosses but supported by the broader backdrop.

The Bank of Canada held its key rate as expected. The neutral stance gave the loonie little fresh direction.

Across the G7 and beyond, the week's central bank sweep delivered no surprises on the decision itself. The cumulative shift in forward guidance, though, is the story. The tone tilted toward inflation risk over growth risk in most jurisdictions. The gap between the Fed's patience and the rest of the G10 has widened, and it is now the dominant driver across the major pairs.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBPUSD | 1.3436 | Uptrend |

| EURUSD | 1.1558 | Range/Up |

| EURGBP | 0.8621 | Downtrend |

| USDJPY | 158.39 | Down |

| AUDUSD | 0.7091 | Uptrend |

| NZDUSD | 0.5882 | Range |

| GBPJPY | 212.32 | Range/Up |

| DXY | 99.43 | Soft, upward bias |

(Rates indicative at time of writing.)

Market Lookahead

Sat, 21 Mar

- USD - Fed Powell Speech

Mon, 23 Mar

- EUR - Eurozone Consumer Confidence (Mar)

- AUD - S&P Global PMI’s (Mar)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.