Payroll Miss, Oil Surge: What’s Next for the Fed?

5 min read

Share

Friday's jobs disaster and a weekend escalation in the Gulf have handed central banks a problem with no clean answer. Both mandates are now in conflict at once.

The US economy lost 92,000 jobs in February against a forecast of positive 59,000, then December was revised from +48,000 to -17,000. That is a deteriorating trend, not a one-month miss.

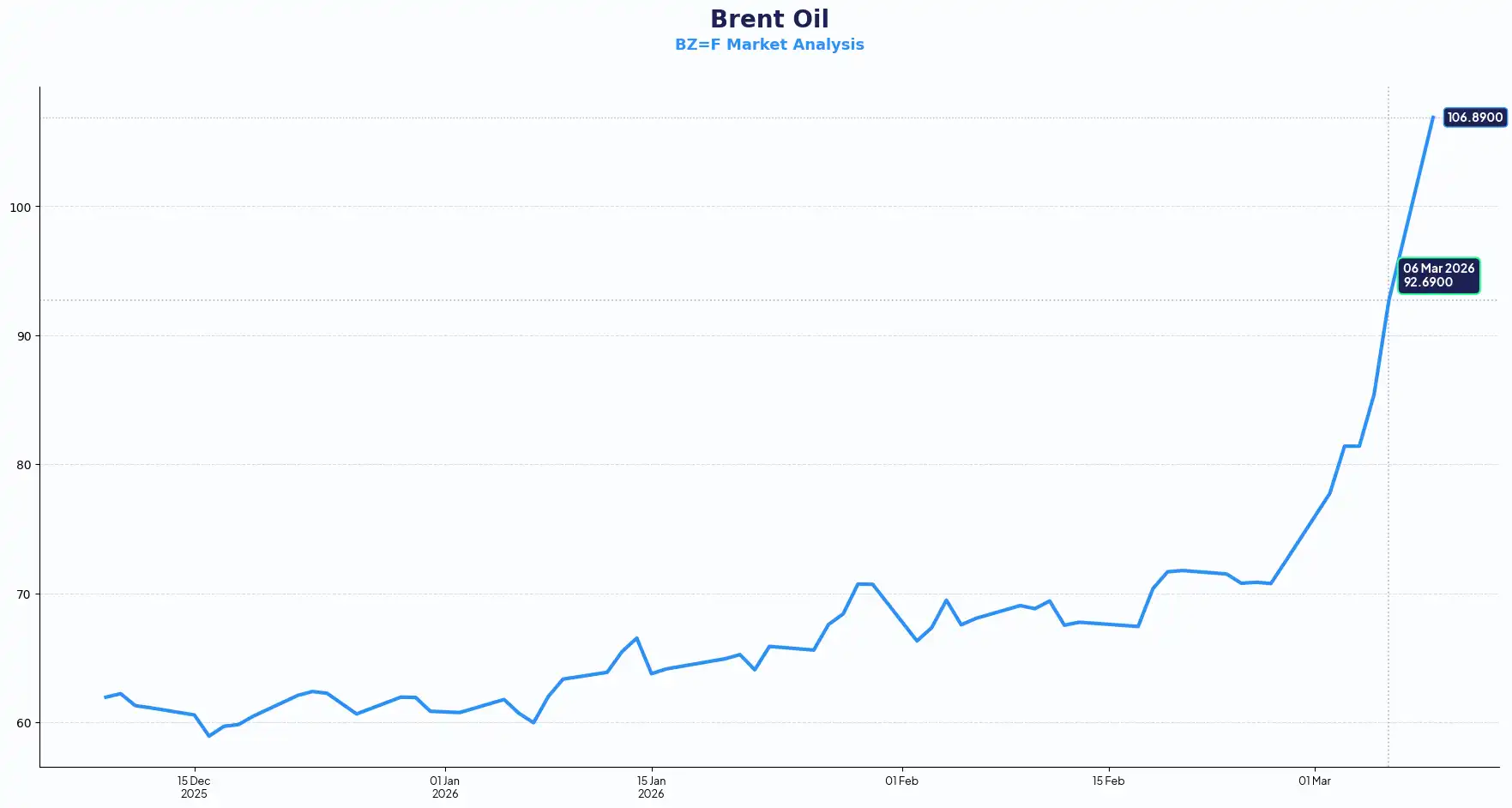

It would have been the story of the week. It was not even the biggest story of the weekend.

Israeli forces struck Iranian oil infrastructure on Saturday for the first time since the conflict began. Brent crude closed Friday at $92.69. By Monday's Asia open it was at $107.53, a 16% overnight jump, and hit $119.50 intraday. The Strait of Hormuz remains closed. Iraq has shut in 1.5 million barrels per day. Qatar's energy minister put $150 on the table as a live scenario, not a tail risk.

Both of our goals are risks now." - Mary Daly, Federal Reserve Bank of San Francisco, 6 March 2026

Weak jobs push toward cuts. $110 oil pushes against them. The Fed is in blackout. March hold is certain. June cut probability sits at 51%, down from above 70% earlier in the week.

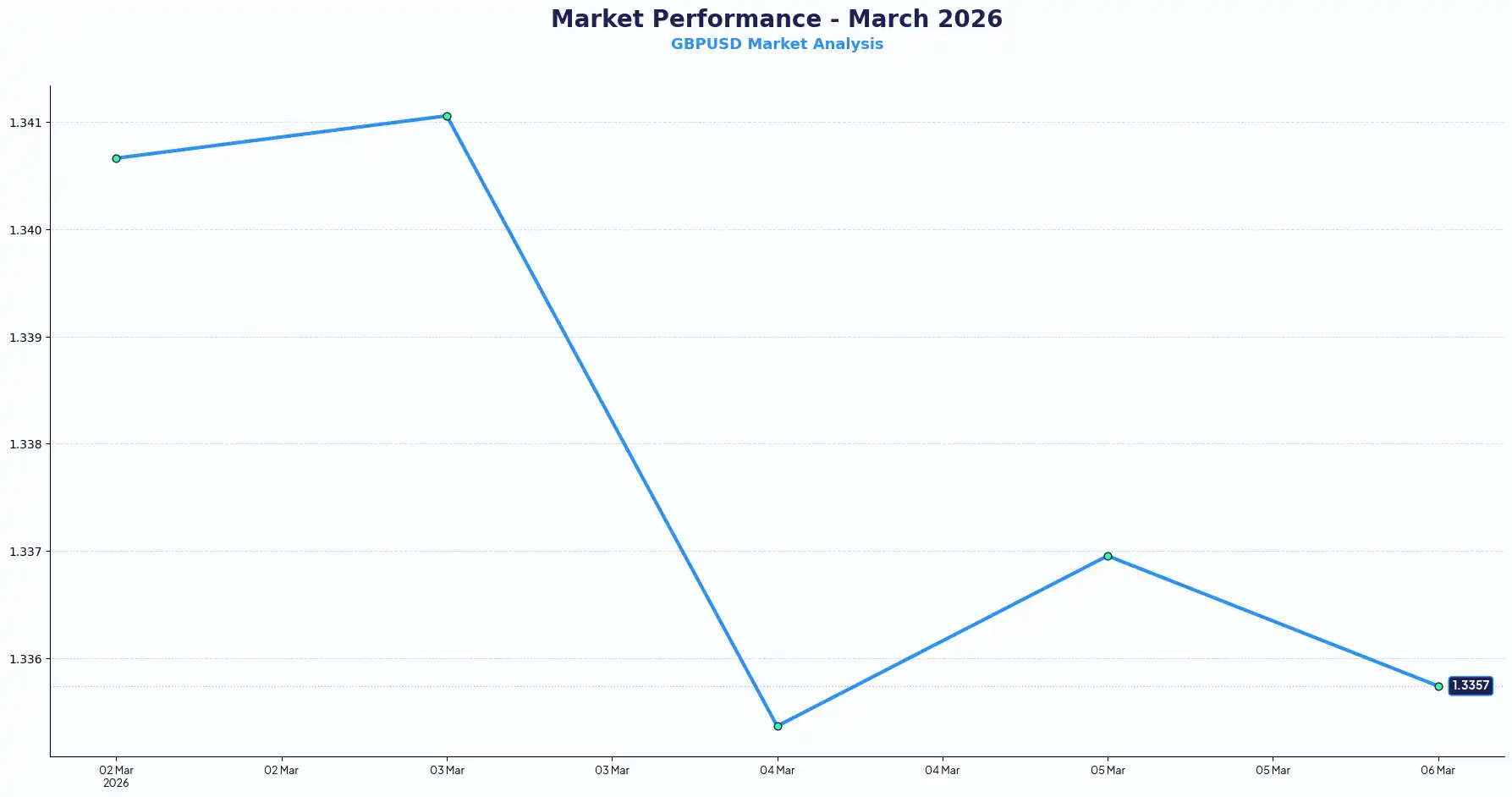

STERLING: SQUEEZED FROM BOTH SIDES

GBP/USD hit 1.3302, a three-month low. The UK is a net energy importer, so $110 oil is not a windfall. It is an inflation shock arriving on top of an already-weak growth outlook. UK gilt yields surged above 4.60% on the week, up more than 40 basis points and the largest single-week gilt move since the 2022 Truss crisis. Bond markets are not treating this as temporary noise.

BoE March cut probability collapsed from 86% to below 20% in five trading days, and the OBR's 2026 growth forecast of 1.1% was set before any oil shock was in the picture. Support at 1.3250–1.3300 is the level to watch. A break below opens 1.3131. Recovery through 1.3420 needs either an energy de-escalation or a BoE pivot. Neither is imminent.

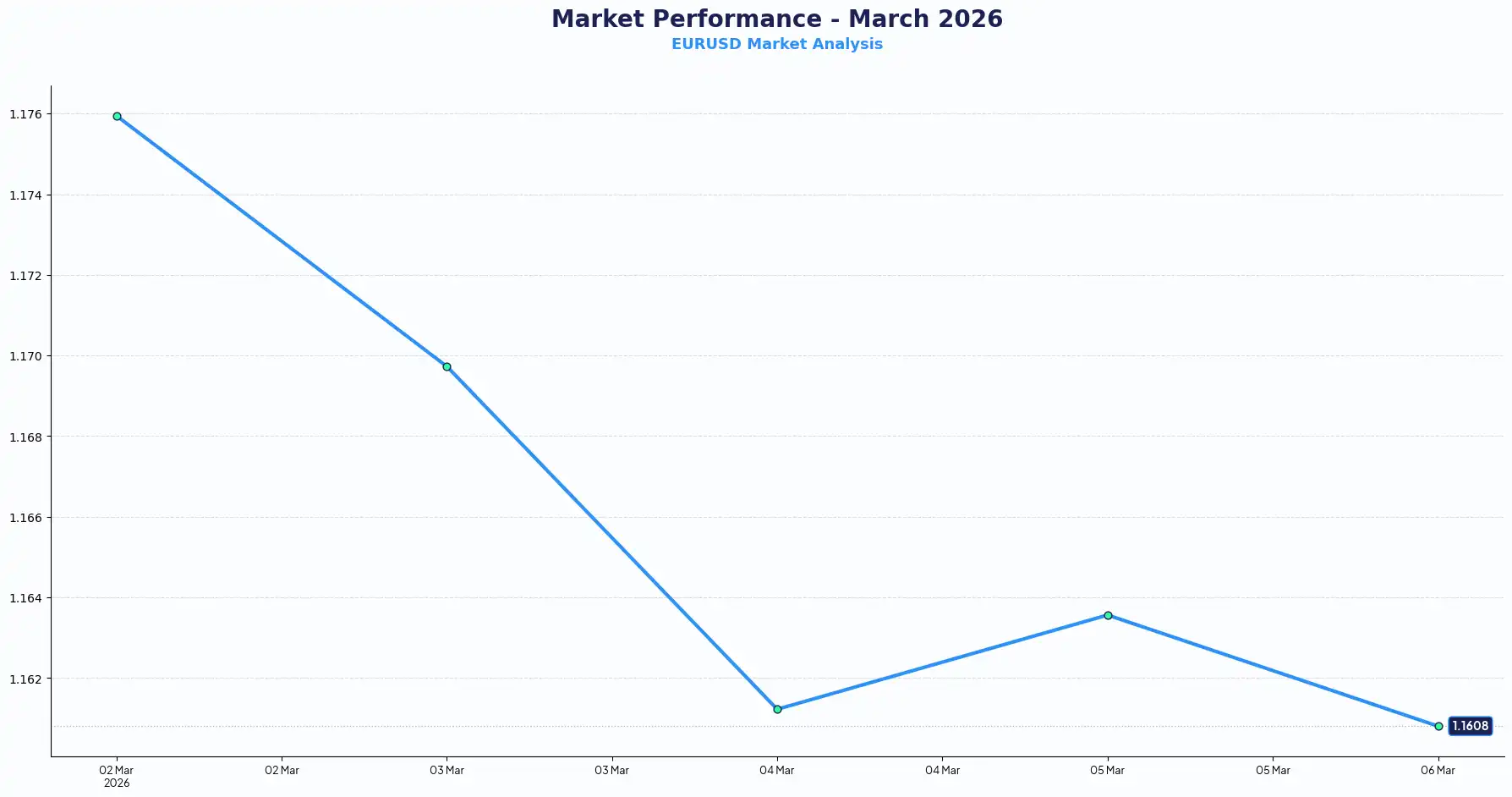

EURO: MOST EXPOSED IN THE ROOM

EUR/USD hit 1.1514, its lowest since late November. Europe's dependence on Middle Eastern LNG is structural, and the Strait of Hormuz disruption does not resolve on the back of a PMI beat. Eurozone Q4 GDP was revised down to 0.2% quarter-on-quarter. Full-year 2025 growth trimmed to 1.4%. The backdrop was already thin before oil moved.

Notably, ECB rate hike pricing has appeared for the first time this cycle. Markets are assigning 55% probability to a July hike, 85% by December. This is not ECB guidance. It is oil doing its own inflation arithmetic. Key support at 1.1500; a close below exposes 1.1390. First resistance sits at 1.1580.

DOLLAR: THE SAFE-HAVEN ARGUMENT WINS

DXY dipped to 98.87 on the payrolls release, then recovered to 99.50 by Monday's open. The reason is visible in one number: Brent closed Friday at $92.69 and opened Monday at $107.53. A 16% overnight jump in oil prices overwhelmed the rate-cut logic of a historic jobs miss. US 10-year Treasuries opened at 4.19%, pulled higher by oil's inflation signal. When the dollar strengthens on bad economic data, financial conditions tighten regardless of what the Fed says.

JPY, AUD, CAD: THREE DIFFERENT POSITIONS

USD/JPY at 158.72. Japan imports 95% of its oil from the Middle East. The yen's safe-haven status does not apply in a Gulf supply shock. Finance Minister Katayama flagged intervention with the strongest language in months. The 160 level is 127 pips away and markets are treating it as a hard ceiling.

AUD/USD broke below 0.70, hitting 0.6964 before settling near 0.6994. Domestic fundamentals remain solid: Q4 GDP beat, RBA hiked in February. But the ASX fell 4.15% on Monday and speculative long positioning leaves the currency exposed to further deleveraging. RBA decision is 17 March.

USD/CAD fell to 1.3567. Canada is a net oil exporter outside the conflict zone. Two consecutive weeks of CAD strength against a broadly bid dollar is a signal, not noise. The BoC decision is on 18 March.

RATES SNAPSHOT | Mon 9 March, early European session

| Pair | Fri 8:30 AM | Mon AM | Move | Near-term lean |

|---|---|---|---|---|

| EUR/USD | 1.1606 | 1.1514 | −92 pips | Downside risk |

| GBP/USD | 1.3354 | 1.3302 | −52 pips | Downside risk |

| USD/JPY | 157.50 | 158.72 | +122 pips | Yen under pressure |

| AUD/USD | 0.7035 | 0.6994 | −41 pips | Downside risk |

| USD/CAD | 1.3675 | 1.3567 | −108 pips | CAD supported |

| DXY | 99.07 | ~99.50 | +0.4% | Safe-haven bid |

(rates as at the time of writing)

FX PLAYBOOK

The following reflects observations on current market conditions for informational purposes only. It does not constitute advice, a recommendation, or a personal suggestion to act. Senior FX dealers may approach these conditions in the following ways, based on typical market practice.

Sterling: 1.3250–1.3300 is the zone to watch. A daily close below likely triggers fresh selling toward 1.3131. Bounces toward 1.3420 without a geopolitical catalyst tend to attract sellers.

Euro: 1.1500 is the line. Options interest is concentrated at and below that strike. A closing break opens the move toward 1.1390.

USD/JPY: 160.00 is treated as a hard ceiling. Katayama's explicit intervention warnings this week are not background noise. Most desks carry hedges against unannounced MoF action.

CAD: CAD is holding against a broadly bid dollar, and that divergence is worth watching. Canada's oil-exporter status is acting as insulation while the conflict persists.

Watch this week: US CPI Wednesday (consensus 2.4%). A print above 2.6% reprices, June cut odds sharply lower. RBA decision 17 March, BoC 18 March.

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.