MARKET OUTLOOK (GBP, EUR & USD) MARCH 2026

7 min read

Share

GBP

The pound lost ground in February, notching its biggest monthly decline against the greenback since last October, retreating substantially from the cycle highs north of 1.38 printed at the end of January, to end the second month of the year just south of the 1.35 figure.

These losses were also seen in the crosses. GBP/EUR shed more than 1% on the month, giving up all of January’s gains and more, in what proved to be the pound’s worst month against the common currency since last summer, taking spot to YTD lows.

This GBP weakness had a few driving forces, though a more dovish BoE policy outlook is undoubtedly the primary one.

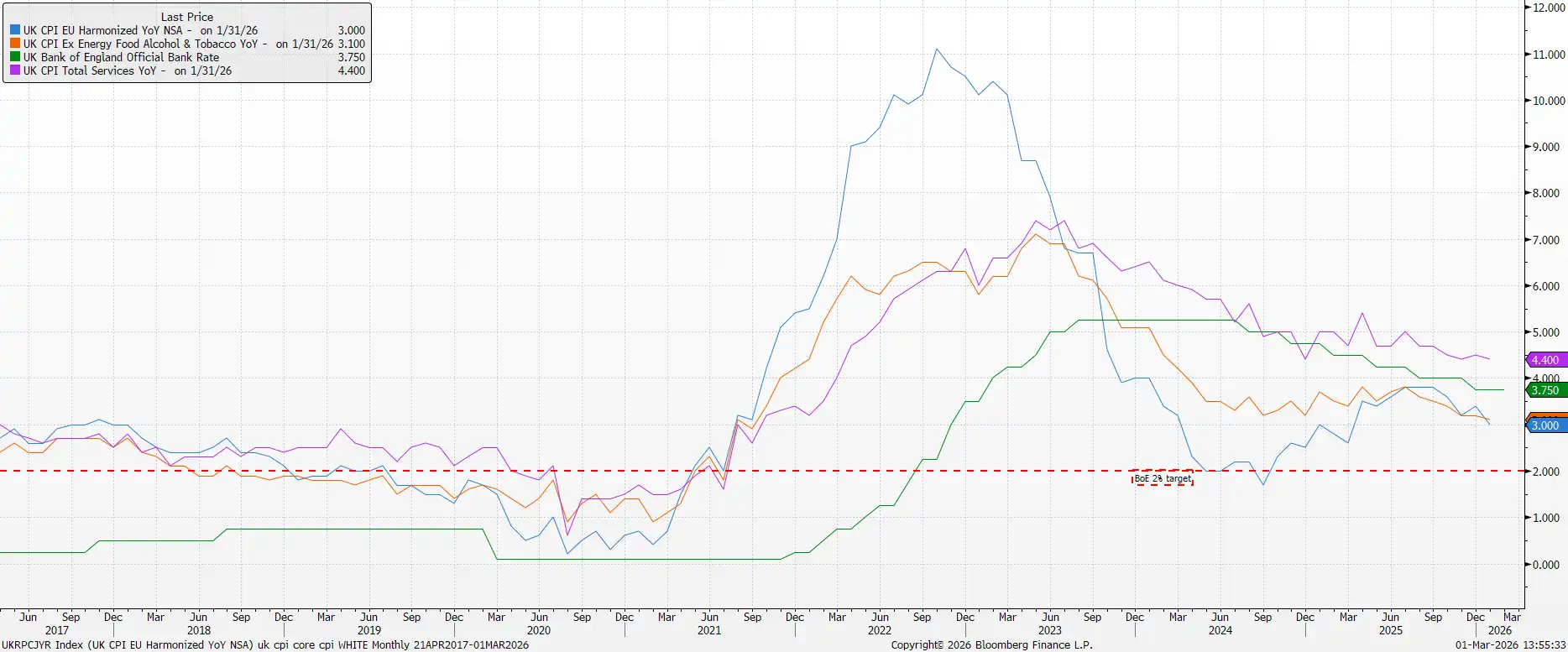

While the MPC held Bank Rate steady at 3.75% at the February meeting, the confab was considerably more dovish than expected. Not only did policymakers vote by the narrowest possible 5-4 margin in favour of standing pat, but the accompanying policy statement explicitly referenced a high likelihood of further Bank Rate cuts in the near future. Furthermore, the Bank’s latest economic forecasts projected the 2% inflation aim being achieved this spring, as much as a year earlier than had previously been anticipated, with prices then set to remain at that target level for the remainder of the three year forecast horizon. All this leads swaps to now discount 52bp of easing by year-end, compared to around 38bp a month ago.

Recent data has reinforced the Bank’s dovish pivot. Headline CPI rose 3.0% YoY in January, the slowest pace since last March, while there was a welcome cooling in underlying inflation metrics – core CPI rose 3.1% YoY, a fresh cycle low, while services CPI rose 4.4%, equalling the slowest pace seen this cycle. Importantly, the January inflation report provided little evidence to cast doubt on the aforementioned forecast of the inflation target being hit this spring, with further energy and food disinflation in the pipeline.

Simultaneously, the risks of price pressures proving persistent have continued to recede, as a significant margin of labour market slack continues to emerge.

Headline unemployment rose to 5.2% in the three months to December, while PAYE payrolls fell for the fifth straight month as the new year got underway. In addition, private sector earnings growth has now fallen to roughly target-consistent levels, while regular pay growth for the entire economy at 4.2% YoY marks the slowest such pace since August 2024. All this, in turn, should give the MPC confidence to pull the trigger on a 25bp cut at the March meeting.

Besides monetary policy, activity data broadly surprised to the upside last month, though with plenty of caveats still being required. Retail sales, for instance, rose 1.8% MoM as the year got underway, marking the biggest MoM increase since May 2024, though the figure was skewed substantially higher by a surge in purchases of precious metals and antiques. Similar applies to the latest round of PMI surveys where, despite the composite output metric printing a 22-month high, the report also showed overall employment having declined for the 17th month running.

Finally, political uncertainty continues to cloud the outlook. While the ʻSpring Statement’ in early-March is likely to be as much of a ʻnon-event’ as any fiscal statement possibly can be, with fresh policy announcements very thin on the ground indeed, PM Starmer’s position remains a perilous one. Having, just about, seen off an internal Labour Party rebellion in mid-February, the PM’s position has once again been weakened by defeat in the recent Gorton & Denton by-election. Though the working assumption remains that Starmer will stagger on until after the May local elections, any significant policy announcements in the meantime are highly unlikely, given Starmer’s lack of any political capital at the current juncture.

EUR

The common currency didn’t really do especially much last month, with both realised and implied volatility remaining at historically low levels, and fresh catalysts distinctly lacking too. as a result, although the EUR did notch its first losing month against the greenback since last October, this was only an 0.3% decline, and in any case keeps spot well within a tight 1.1750 – 1.1900 range.

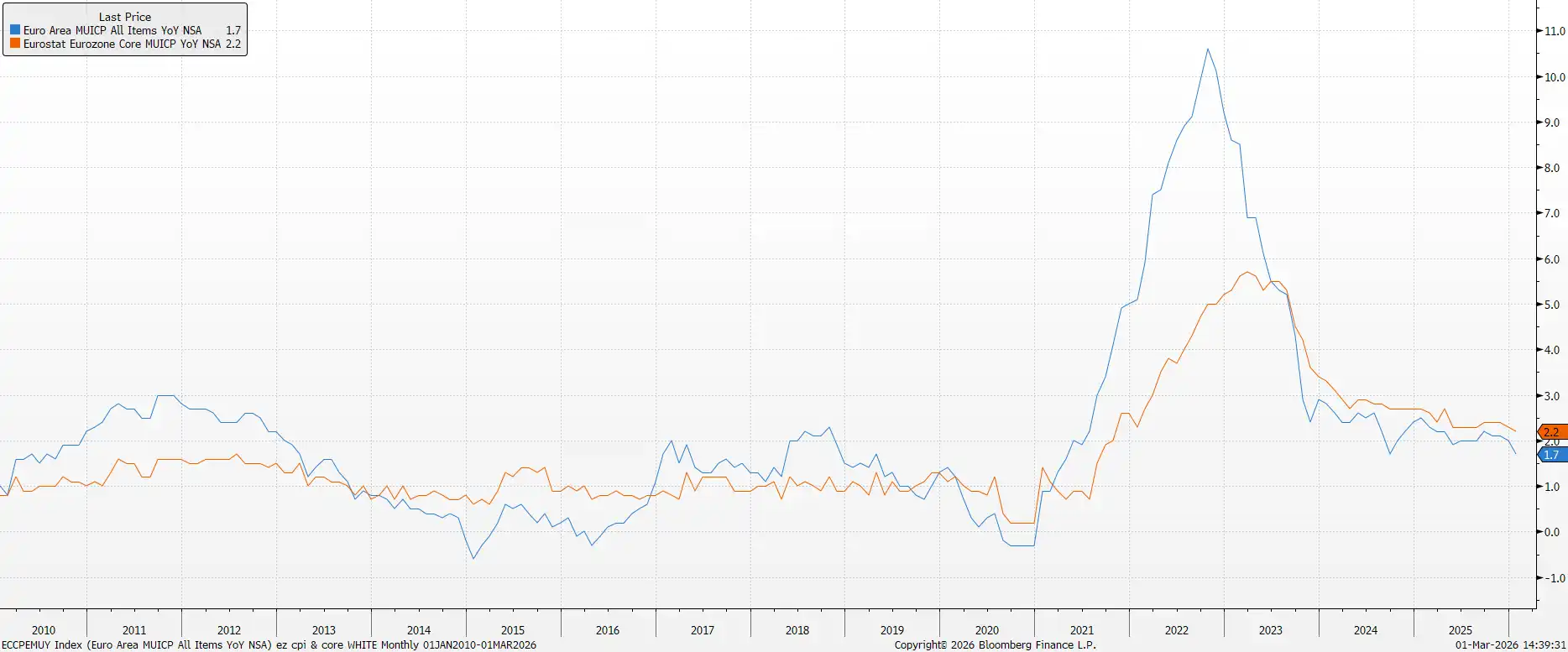

As noted, domestic developments were notably thin on the ground throughout the month. The first ECB confab of the year passed without event, as the Governing Council held all policy settings steady, maintaining the deposit rate at 2.00%, while reiterating that policy is in a ʻgood place’, and that a ʻdata-dependent’, ʻmeeting-by-meeting’ approach will continue to be taken moving forwards. For all intents and purposes, though, the ECB’s easing cycle is now at an end, with the GC set to stand pat for the foreseeable future.

This is despite inflation having undershot the 2% target in January, and likely continuing to do so for the remainder of the year. For the time being, at least, the ECB are content to look through this undershoot, with it being driven largely by a base effect in energy prices, which will drop out of the data as the year progresses. In any case, core inflation continues to run marginally above target, at 2.2% YoY.

In any case, perhaps the bigger concern when it comes to the ECB at the moment is the issue of leadership. Media reports indicate that President Lagarde may be seeking to stand down early, before the scheduled expiry of her term in October 2027, potentially in order to allow outgoing French President Macron an opportunity to play a role in choosing her successor. Despite being given ample opportunity, Lagarde has refused to explicitly deny that an early exit could be on the cards, with such a move likely resulting in significant uncertainty as a succession battle plays out, potentially posing a headwind to the currency as a result.

In the meantime, though, the EUR is likely to be driven largely by external developments, with the ECB sitting on the sidelines for the time being, and market participants likely lacking conviction to move spot out of the tight recent trading range, especially as evidence of a fiscal boost – that most had expected coming into the year – currently remains elusive.

USD

The greenback traded marginally firmer against a basket of peers last month, with the Dollar Index (DXY) notching its first positive monthly return since last October, albeit while remaining within the broad 96 – 100 range that’s now been in place since last summer.

Not helping this relative lack of volatility is the monetary policy outlook, with the Fed having shifted firmly towards a ʻwait and see’ approach at the January meeting, and with policymakers having given little inclination in recent public remarks that such a stance is likely to shift any time soon.

In fact, recent data has likely provided policymakers with a degree of reassurance when it comes to the employment backdrop. Unemployment unexpectedly fell to 4.3% in January, while headline nonfarm payrolls rose +130k, the largest MoM jump in over a year. Furthermore, the 3-month moving average of private sector payrolls excluding healthcare, a gauge of cyclical job creation, is now at its highest level since ʻLiberation Day’ last year, providing a further signal that the labour market may be beginning to stabilise.

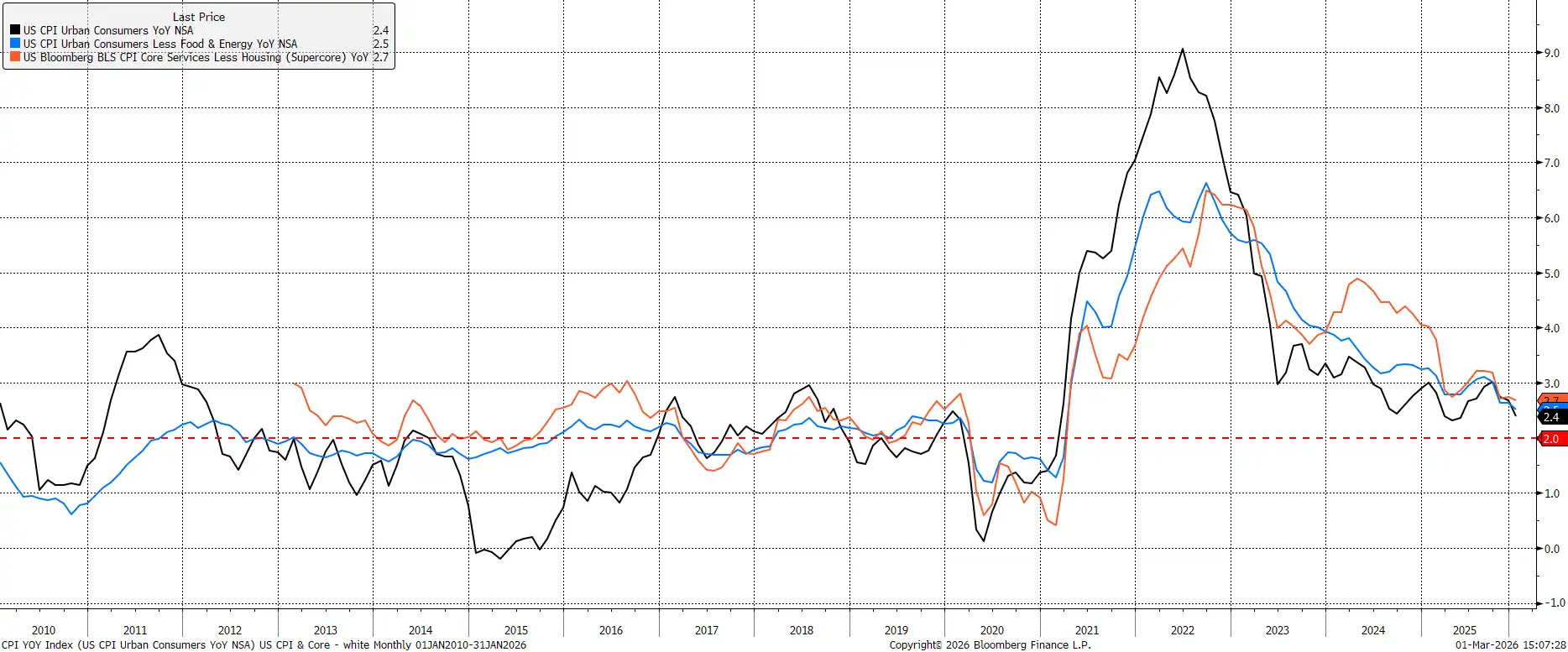

Along with this, the gradual disinflation process continues, albeit with the caveat that CPI figures remain skewed lower by the impact of last year’s government shutdown. Even with that in mind, the 2.4% YoY headline CPI print in January was the lowest level since March, while core CPI slipped to a cycle low. Furthermore, core goods prices rose at their slowest pace in six months, providing further evidence that the pass-through of tariffs in the form of higher consumer prices is likely at an end.

Zooming out, with the Fed likely to stand pat at least for the final two meetings of Chair Powell’s term at the helm, other driving forces are likely to impact the buck over the course of the month ahead.

Of course, geopolitical events are a key focus, with a joint US-Israeli operation having now begun in the Middle East, with the aim of regime change in Iran. While it remains highly uncertain, at the present juncture, how exactly that conflict pans out, it seems plausible that an increase in geopolitical risk would spark some haven demand for the greenback, at least in the short-term. On that note, the ʻsell America’ hyperbole appears to have considerably died down in recent weeks, though participants do continue to take a relatively dim view of the policy volatility which continues to emanate from the White House.

Click here for an instant quote or contact us for a free foreign exchange health check, guaranteed to save you money.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.