GBP/USD Buoyed Amid a Bearish USD

10 min read

Share

GBP/USD edged higher to 1.3760 as investors brace for addresses by Bank of England (BoE) Governor Andrew Bailey and Federal Reserve (Fed) Chair Jerome Powell. A mix of concerns about the chaotic US trade policy, fears over the country's mounting fiscal debt, and rising expectations that the Federal Reserve (Fed) will cut interest rates at least twice before year's end dampen market sentiment around the US dollar. Fears about Trump's Tax Bill, which is expected to add $3.3 trillion to the US fiscal debt, have resurfaced in the market. Anxiety over a potential debt crisis is eroding the idea of US exceptionalism and adding pressure on the US dollar. Trump has expressed frustration over trade talks with Japan, and Treasury Secretary Bessent warned that the US might impose higher tariffs on July 9 despite ongoing negotiations. Regarding monetary policy, the US President has continued criticising Fed Chair Powell, suggesting that US interest rates should be between Japan's 0.5% and Denmark's 1.75%. These comments raise doubts about the independence of the central bank and threaten the US dollar's position as the world's reserve currency. The Chicago Purchasing Managers' Index (PMI) came in at 40.4, compared to the previous 40.5, well below the forecast 42.7, indicating contraction in the region's manufacturing sector. Atlanta Fed President Raphael Bostic acknowledged ongoing uncertainty surrounding tariffs and their inflationary effects, emphasising the Federal Reserve's capacity to remain patient given the resilience of the labour market.

On the sterling side, market expectations that the BoE will cut interest rates at the upcoming policy meeting to address slow economic growth and a weaker labour market influenced the pound. Data showed the core current account deficit, excluding trade in precious metals, slightly fell to £18.6 billion, or 2.5% of GDP, in Q1 2025, a £0.1 billion improvement from the previous quarter's deficit of £18.7 billion. However, including trade in precious metals, the UK's current account deficit increased by £2.4 billion to £23.5 billion, or 3.2% of GDP. The total trade deficit, excluding precious metals, decreased to £7.5 billion (1.0% of GDP) from £10.2 billion in the previous quarter. This decline was mainly due to a drop in the goods trade deficit to £55.3 billion, with the services trade surplus also shrinking to £47.8 billion. Meanwhile, the UK economy resumed growth in Q1, with final GDP data from the Office for National Statistics confirming a 0.7% quarter-on-quarter rise and a 1.3% year-on-year increase. The S&P Global UK Manufacturing PMI rose to 47.70 in June from 46.40 in May 2025. Real household disposable income fell by 1.0%, the sharpest decline since early 2023, as rising prices and taxes eroded consumer spending power. The household saving ratio also decreased to 10.9% from 12.0%, reflecting savings being used to support spending.

Apart from the speech by BoE Governor Andrew Bailey, ISM Manufacturing PMI, US labour market data, and Fed Chair Jerome Powell's speech will influence the GBP/USD exchange rate.

EUR/JPY Wobbles Following Eurozone Inflation Report

EUR/JPY struggled near 168.91, following the release of key economic data from the Eurozone. The HCOB Eurozone Manufacturing PMI inched higher to 40.5 in June 2025 from 49.4 in the previous month, revised slightly upwards from the flash estimate of 49.4, but remained well below the initial forecast of 49.8. The Eurozone Harmonised Index of Consumer Prices (HICP) increased by 2% annually in June, following a 1.9% rise in May, aligning with market expectations. The core HICP rose 2.3% YoY in June, matching the May figure and meeting the estimate. On a monthly basis, the bloc's HICP inflation was 0.3% in June, compared to 0% in May. The core HICP increased by 0.4% MoM in the same period, after no change in May. On Monday, Germany's Federal Statistical Office announced that import prices fell by 1.1% YoY in May, surpassing the market expectation of 0.8%. Germany's initial consumer price figures for June are expected to show a slight increase, with a 0.2% monthly rise and a 2.2% annual rate, up from 0.1% and 2.1%, respectively, in the previous month. Inflation in Germany, as measured by the Consumer Price Index (CPI), edged lower to 2% in June from 2.1% in May, according to Destatis' flash estimate on Monday. On a monthly basis, the CPI remained unchanged, versus the market expectation of a 0.2% increase. The Harmonised Index of Consumer Prices in Germany, the European Central Bank's preferred inflation measure, declined to 2% annually after rising 2.1% in May. This reading was below the analysts' estimate of 2.2%. The HCOB Italy Manufacturing Purchasing Managers Index dipped to 48.4 in June from 49.2 in May.

On Tuesday, Boris Vujčić, a policymaker at the European Central Bank (ECB), stated that the bank "faces the possibility of new inflation shocks." He also mentioned that "higher defence spending will contribute somewhat to inflation pressures." Pierre Wunsch, another ECB policymaker, said that "if a move is needed, it would be downward." Gediminas Šimkus noted, "I don't know if we'll have all the information we need by September, but I remain open to every possibility." He added, "I believe any move, if it occurs, is more likely toward the end of the year." Meanwhile, Governing Council member Jose Luis Escriva emphasised that "a symmetric 2% goal should remain ECB's primary guide." ECB's de Guindos commented on facing "brutal uncertainty," indicating that growth in Q2 and Q3 could be stagnant and that all options should be considered. Chief Economist Philip Lane said deviations from the 2% inflation target could be larger on either side.

On the yen's front, the upbeat Japanese Tankan survey and BoJ rate hike bets inject market volatility into the currency. Business sentiment among Japan's major manufacturers unexpectedly improved in the second quarter of 2025. This positive update supports the Japanese yen and creates a headwind for the cross. The Tankan Large Manufacturing Index increased to 13.0 in Q2 from 12.0 in Q1, surpassing the market consensus of 10.0. Additionally, the Large Manufacturing Outlook stayed steady at 12.0 in Q2, ahead of the expected 9.0. On Tuesday, Bank of Japan's (BoJ) new board member Kazuyuki Masu commented that he wants to scrutinise how prices move after the recent spike in the price of rice moderates. Regarding interest rate decisions, he added that recent economic conditions suggest we're not in a position where the BoJ can rush into raising interest rates and that it must move cautiously, keeping a close eye on various data.

Broader market sentiment around ECB President Lagarde and BoJ Governor Kazuo Ueda's speech, along with the Eurozone inflation report, will shape the market sentiment around the EUR/JPY exchange rate.

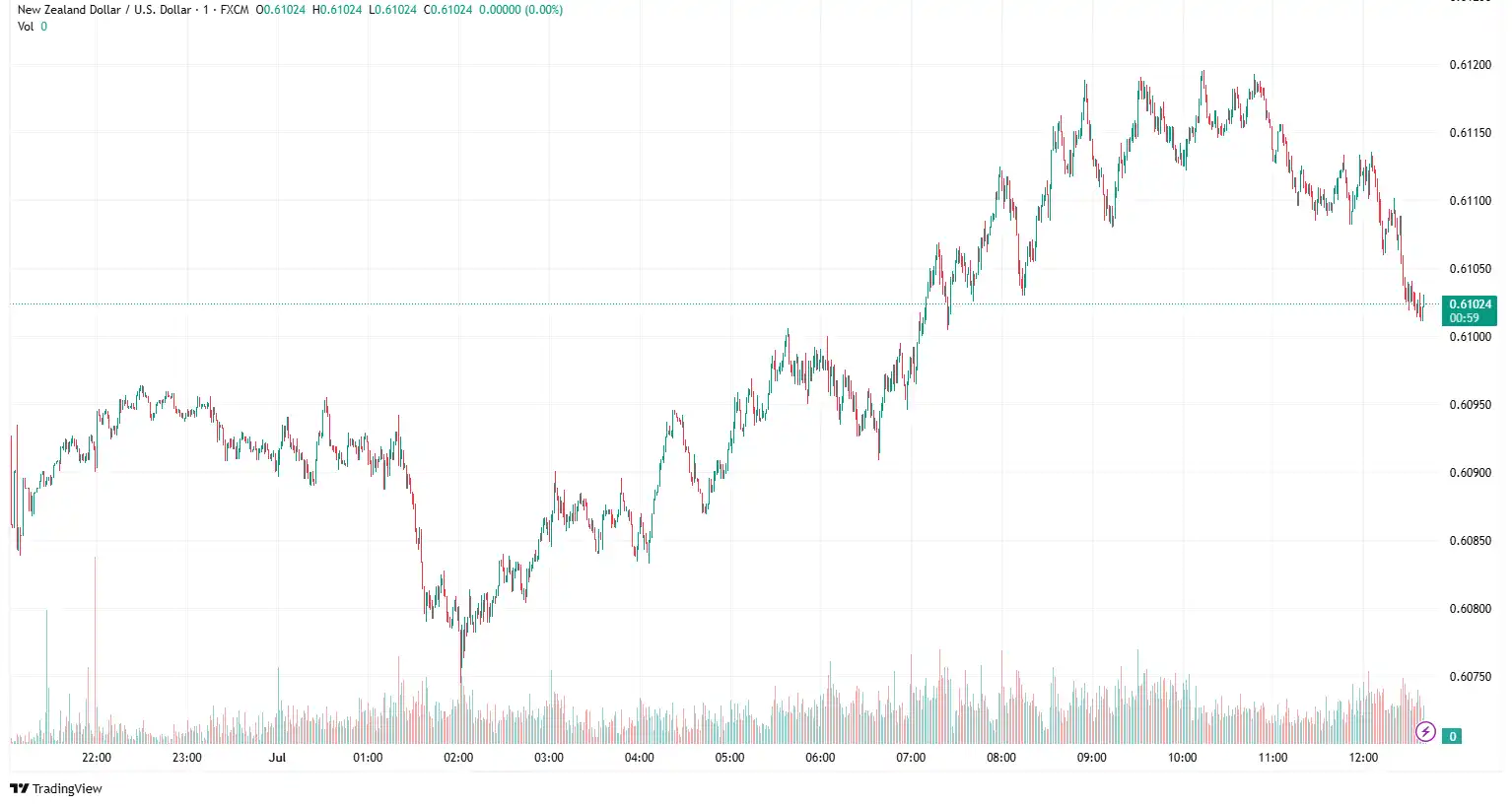

NZD/USD Climbs Following NZIER Business Confidence

NZD/USD gained momentum near 0.6105 after the release of the key economic data from New Zealand and its close trading partner, China. NZIER Business Confidence increased by 22% quarter-over-quarter in the second quarter, up from 19% previously. Seasonally adjusted Building Permits rose by 10.4% month-on-month in May, reaching a total of 3,151 units after seasonal adjustment. The ANZ headline index increased from 36.6 to 46.3, while firms' Own Activity Outlook improved from 34.8 to 40.9. Inflation expectations remained steady at 2.71%. While the labour market shows a monthly gain, the total number of filled jobs remains near a 28-month low, marking April's data as the weakest since January 2023. Growth forecasts for Q2 remain subdued. ASB predicts a 0.3% increase, while the Reserve Bank of New Zealand's (RBNZ) GDP nowcast indicates just 0.1% growth. China's NBS Manufacturing Purchasing Managers' Index (PMI) rose to 49.7 in June, up from 49.5 in May, aligning with market expectations for the month. The NBS Non-Manufacturing PMI increased to 50.5 in June from 50.3 in May, meeting the forecast of 50.3. China's Caixin Manufacturing Purchasing Managers' Index (PMI) improved to 50.4 in June from 48.3 in May, surpassing the market forecast of 49.0. Finance Minister Nicola Willis warned last week that tariff uncertainty and Middle East tensions have lowered business sentiment and investment, stating it will be "very challenging to sustain the previous level of growth." The market anticipates a sharp rise in the jobless rate in the second and third quarters as US President Donald Trump's unpredictable trade policies are expected to erode business confidence and influence the economy. Moreover, the Reserve Bank of New Zealand's (RBNZ) monetary stance could inject market volatility into the New Zealand dollar.

Conversely, positive market sentiment after news that the US was reducing its tariff negotiation targets affected the US dollar. Nonetheless, efforts by the US Senate to pass Trump's tax cut and spending bill, which faces internal party disagreements over its estimated $3.3 trillion increase in the national debt, caused market uncertainty due to fiscal concerns, leading to a decline in the US dollar. On the policy front, US President Donald Trump has formally complained about high interest rates to Federal Reserve (Fed) Chair Jerome Powell. The Fed has adopted a cautious wait-and-see approach regarding how the US economy will handle potential fallout from the Trump administration's erratic trade policy. President Trump has steadily increased hostile rhetoric towards the Fed in recent weeks, culminating in a formal complaint to the Fed's head on Monday.

Upcoming US employment data and US June ISM Manufacturing Purchasing Managers Index (PMI) data will significantly influence the NZD/USD exchange rate.

GBP/JPY Sinks Amid Diminishing BoJ Expectations

GBP/JPY dropped to near 196.91, as the Bank of Japan's (BoJ) Tankan Survey indicated that business confidence among large manufacturers in Japan increased for the first time in two quarters during the April-June period, strengthening the yen. Business confidence among large manufacturers in Japan increased to 13.0 in the second quarter (Q2) of 2025, up from 12.0 in Q1, according to the Bank of Japan's quarterly Tankan survey on Tuesday. This reading exceeded the market consensus of 10.0. Additional details show that the Manufacturing Outlook for the second quarter was 12.0, unchanged from the previous quarter, and stronger than the expected 9.0. Moreover, firms anticipate consumer prices will rise by 2.4% over the next three years and by 2.3% annually over the next five years. The Statistics Bureau of Japan reported this Friday that the headline Tokyo Consumer Price Index (CPI) increased by 3.1% Year-on-Year (YoY) in June, compared to 3.4% in the previous month. The core measure, which excludes fresh food, slowed from 3.6% YoY in May to 3.1%, against the 3.3% forecast. Additionally, the Tokyo CPI excluding both fresh food and energy rose by 3.1% year-on-year after a 3.3% increase in May. A separate government report showed that retail sales in Japan fell by 0.2% month-on-month (MoM) in May, following an upwardly revised growth of 0.7% in April. Yearly retail sales increased by 2.2% during the reported month, down from an upwardly revised 3.5% rise in April, and below market expectations of 2.7% growth. The data reaffirms expectations that the Bank of Japan may refrain from raising interest rates in 2025, although inflation in Japan's capital city remains well above the central bank's 2% annual target.

Furthermore, signs of a steady increase in domestic inflationary pressures sustain hopes for further rate hikes by the BoJ. Japanese Chief Cabinet Secretary Yoshimasa Hayashi said on Tuesday, "Japan won't do anything to sacrifice the agriculture sector in US trade talks." Earlier, the country's Farm Minister Shinjirō Koizumi noted that they "will continue to work with various ministries towards maximising Japan's national interests in the context of trade negotiations with the US." On Monday, Japan's top trade negotiator, Ryosei Akazawa, stated that he will continue working with the United States to reach an agreement while upholding Japan's national interests. Akazawa stated that he is aware of President Trump's comment regarding his decision not to discuss the auto sector. "It was unfortunate I couldn't meet Bessent this time." Bank of Japan's new board member, Kazuyuki Masu, stated on Tuesday that he plans to examine how prices change once the recent rice price surge stabilises. He also mentioned, "Automobiles are a key part of Japan's exports to the US, so there should be no preconceived notions about their impact on Japan's economy until trade negotiations with the US are completed."

On the sterling front, investors look forward to Bank of England (BoE) Governor Andrew Bailey's speech, seeking fresh insights on the currency. The UK economy grew by 0.7% in Q1, the strongest in a year, while annual growth remained at 1.3%. However, real household income fell by 1.0%, the largest decline since early 2023, and the savings ratio dropped to 10.9%, indicating pressure on consumer finances. Further dampening the outlook, the Current Account deficit widened to £23.46 billion, significantly exceeding expectations.

In today's session, BoE Governor Andrew Bailey and BoJ Governor Kazuo Ueda's speeches will influence the GBP/JPY exchange rate.

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.