Fed Takes Centre Stage as Sterling Loses Ground on Soft CPI

7 min read

Share

UK inflation undershoots, the euro gains on the pound, and the dollar holds ahead of the Fed's first decision under Warsh. Oil's retreat and the US-Iran deal reshape the broader FX landscape, while markets await the Fed and BoE decision next.

GBP: Soft CPI Weighs on Sterling

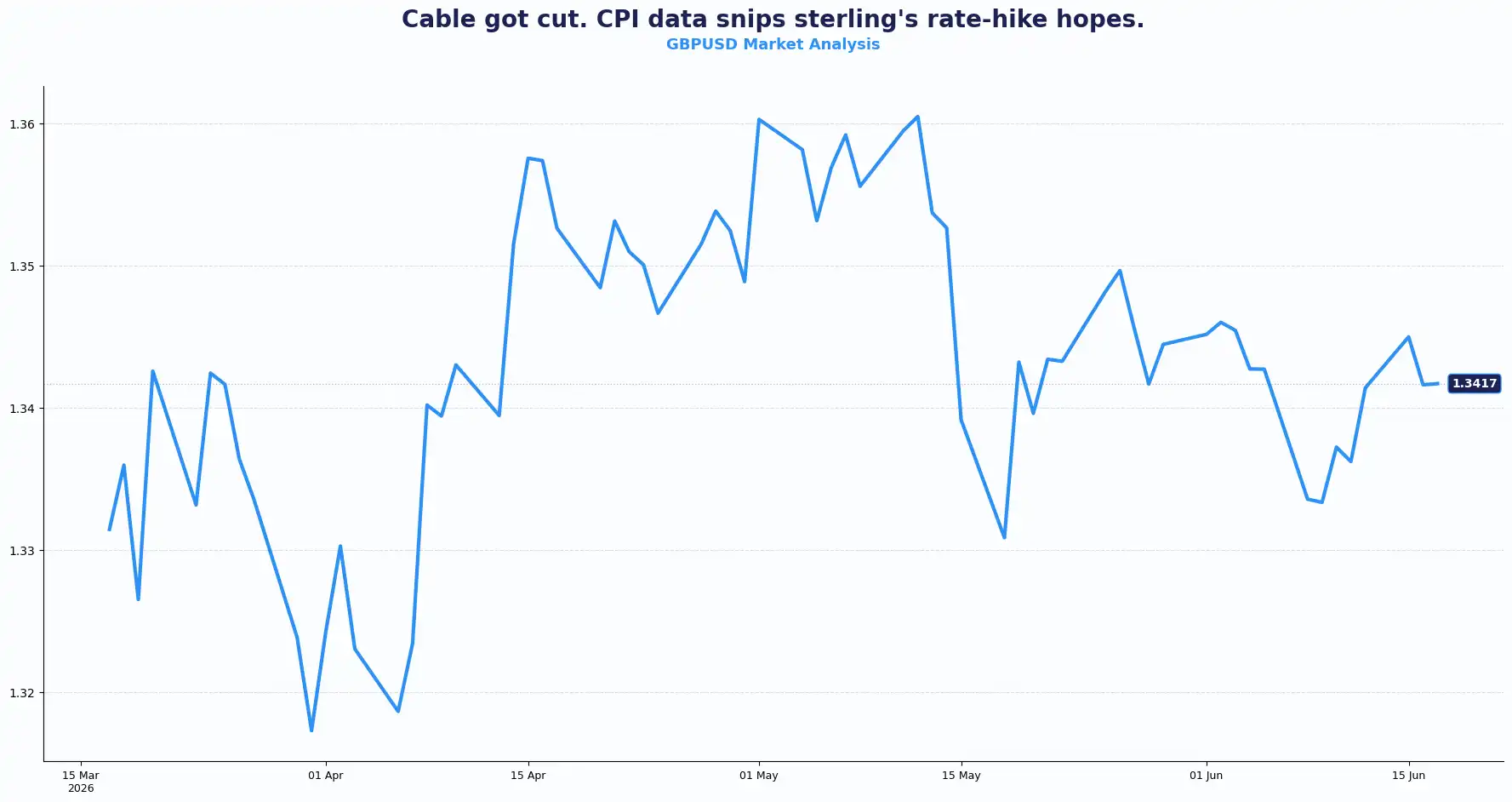

GBPUSD 1.3417 | EURGBP 0.8654

UK inflation printed softer than anticipated in May. The Office for National Statistics confirmed consumer prices rose 2.8% year-on-year, unchanged from April, while the monthly reading came in at 0.2%, well below April's 0.7% and the 0.4% consensus forecast. Core CPI nudged to 2.6% annually, from 2.5% prior, still beneath the 2.7% the market had pencilled in.

The data pushed GBP/USD to weekly lows at 1.3410 before a partial recovery to 1.3431. EUR/GBP climbed to 0.8650, with the euro drawing relative strength from the pound's dip.

The Bank of England (BoE) is expected to hold its rate decision on Thursday. With headline inflation steady and core CPI below consensus, the case for near-term rate action has weakened. Governor Andrew Bailey has indicated the BoE wants more data on whether elevated energy costs tied to Middle East tensions will generate lasting price pressure before it moves. Thursday's UK employment figures will factor into that assessment.

This may lead to a period of a narrower rate differential for sterling against the euro. The pound came into this week with expectations of BoE patience priced in; the softer data reinforces that picture. Cross-rate moves in the EUR/GBP pair have closely tracked the relative policy stance throughout 2025, and Wednesday's session continued that pattern.

The next 48 hours, spanning UK employment data and the BoE rate decision announcement, are the next major catalysts for sterling and its pairs.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3490, 1.3550 and Support sits at 1.3410, 1.3380

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8670, 0.8710 and Support sits at 0.8620, 0.8590

EUR: ECB Keeps Inflation Risks in Focus

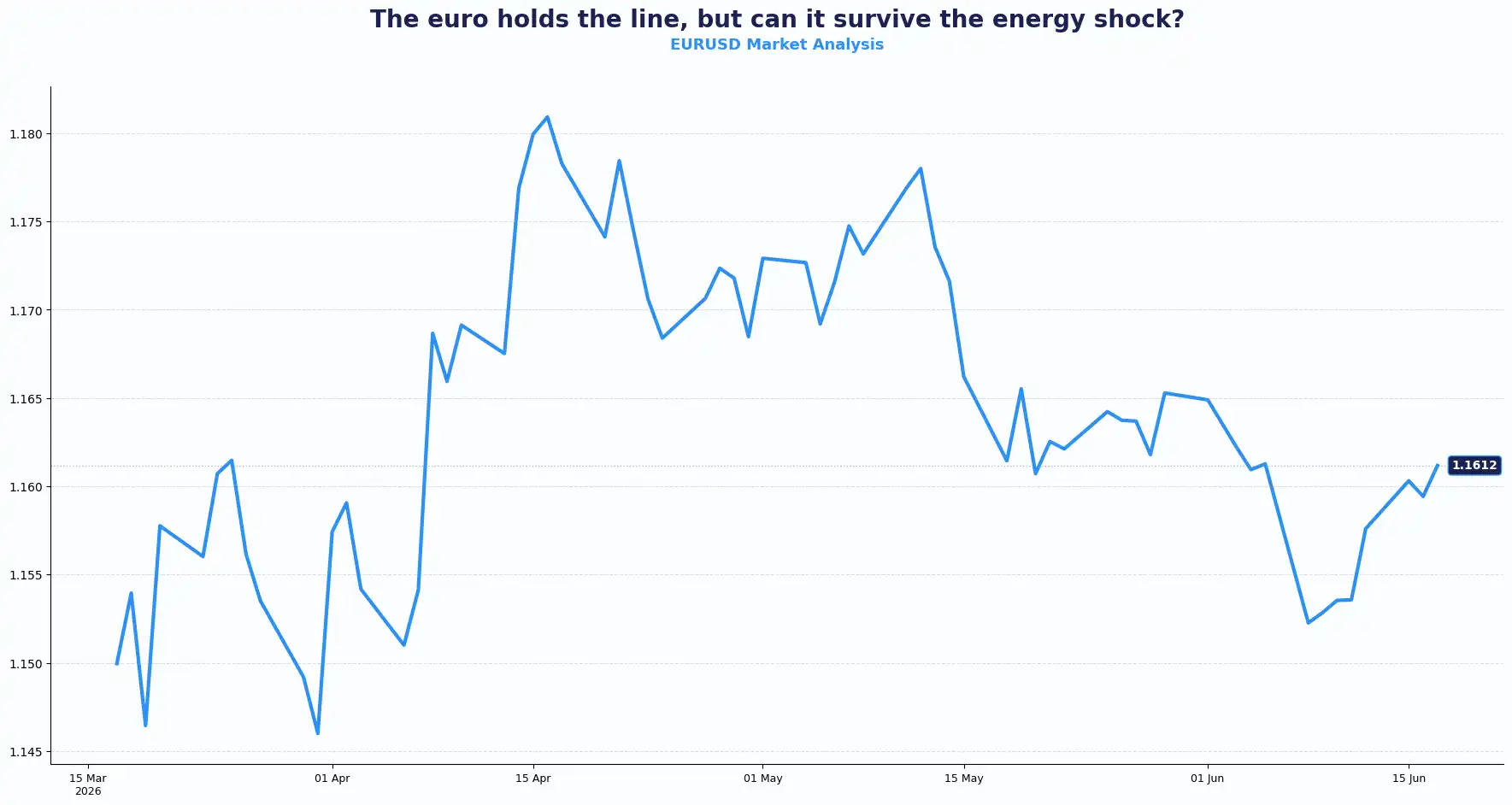

EURUSD 1.1612

The euro held at $1.1612 against the dollar on Wednesday. The European Central Bank (ECB) raised rates last week, the first increase since September 2023, after seven consecutive holds. Chief Economist and Member of the ECB committee, Philip Lane, confirmed the decision was deliberate and data-grounded. Lane cited the war in the Middle East as generating inflationary pipeline pressure, with the current oil price curve sitting between the ECB's baseline forecast and a mild energy shock scenario. He characterised the move as a safe decision, with the Eurozone economy showing resilience and the financial system robust.

What distinguishes the ECB's position from the BoE's is intent. Where Bailey pauses, Lane presses. The ECB's rate hike signals that it views inflation risks as active and addressable through policy tightening. Lane acknowledged the shock is medium-sized, and inflation is unlikely to reach the severity to that of five years ago, but he was clear that it is not invisible, and data dependency cuts both ways for future decisions.

For the EUR/GBP pair, the ECB-BoE divergence has now become a structural feature of the cross, not merely a transient one. The ECB tightening while the BoE holds creates upward pressure on EUR/GBP, which today’s UK CPI data brought sharply into focus. This divergence, rather than day-to-day data noise, represents the underlying driver of the cross's directional move this week.

The EUR/USD pair’s relative steadiness near 1.1600 reflects a different dynamic: the euro and dollar are both caught in a holding pattern ahead of the Fed. Investors will be closely watching the FOMC decision and Warsh’s commentary for further cues on near-term direction for the dollar and the cross.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1650, 1.1700 and Support sits at 1.1570, 1.1530

USD: Warsh's Debut and the Fed's Decision

DXY: 99.50

The dollar eased to a DXY reading of 99.50 on Wednesday as investors lightened safe-haven positioning following confirmation of the US-Iran interim peace deal. The deal's details, including a memorandum of understanding between the two governments, reduced geopolitical risk premiums in crude oil and supported broader risk appetite, dollar-negative in the short run.

The Federal Reserve (Fed) announces its rate decision later today. This is the first FOMC meeting chaired by Kevin Warsh, who replaced Jerome Powell. Markets price in unchanged rates with high conviction. The scrutiny is not on the rate decision itself but on the statement, updated economic projections, and Warsh's tone at the press conference, which might give further cues on dollar direction.

Warsh brings a distinct profile to the chair. His documented view that A.I. carries disinflationary potential, questions about his relationship with the Trump administration's policy preferences, and his stated preference for a trimmed CPI target all leave the hawk-dove read genuinely uncertain. The committee he now leads includes members with varying views. Warsh's first conference may deliver more diplomatic even-handedness than the market's positioning assumes. That repricing, should it materialise, carries implications for the dollar's direction in the second half of this week.

The broader dollar picture this week has been shaped by the US-Iran peace deal and oil prices’ pullback more than the Fed rate expectations alone. With crude retreating and the safe-haven premium unwinding, the dollar has given back some of last week's gains. A "higher for longer" neutral stance from the Fed, as opposed to renewed tightening, could likely keep the DXY in a holding range. Economic resilience alongside gradually easing inflation is the scenario that underpins that outcome.

Other Currencies: JPY, AUD, NZD, CNY

AUDUSD 0.7068 | NZDUSD 0.5830 | USDJPY 160.27 | GBPJPY 215.26 | USDCNY 6.7570

The yen trades at 160.27 per dollar, territory that traders flag as a zone where Japanese authorities have previously intervened. The Bank of Japan (BoJ) raised its policy rate on Tuesday to a 31-year high, a landmark step in its post-deflation normalisation cycle. Despite the historic significance of that move, the rate hike delivered little incremental guidance on the timing of the next step and the yen's weakness persisted.

The BOJ's press conference acknowledged optimism about the Japanese economy but offered no specific forward guidance. The meeting also confirmed Japan is actively diversifying crude oil imports away from the Middle East, though US crude comes at a premium of approximately $10 per barrel above Middle Eastern pricing. That cost differential complicates the inflation picture that the BOJ is trying to navigate.

The Aussie dollar held near $0.7068. The Reserve Bank of Australia (RBA) kept its cash rate at 4.35% on Tuesday, signalling the economy is slowing under tighter financial conditions. The RBA retained a tightening bias, warning it may yet raise rates if inflation does not moderate. Falling oil prices offer the Aussie some support through improved risk sentiment, but simultaneously reduce the probability of further rate hikes, a two-sided dynamic the currency is visibly navigating.

The New Zealand dollar held at $0.5832, after firming overnight. The kiwi's near-term movement tracks risk appetite and commodity pricing closely given its commodity-currency profile.

The Chinese yuan opened at 6.7570 per dollar, hovering near its strongest level in three years. The yuan is up 3.5% YTD. The People's Bank of China (PBOC) set its daily midpoint at 6.8096, weaker than spot, a deliberate signal that the PBOC wants to manage the pace of appreciation rather than allow it to run. Governor Pan Gongsheng confirmed the PBOC will refine its overnight repo and reverse repo operations to improve flexibility. The offshore yuan traded at 6.7565, broadly aligned with onshore levels.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3417 | Bearish |

| EUR/USD | 1.1612 | Neutral |

| EUR/GBP | 0.8654 | Bullish EUR |

| USD/JPY | 160.27 | Yen pressure |

| GBP/JPY | 215.26 | Yen pressure |

| AUD/USD | 0.7068 | Range bound |

| NZD/USD | 0.5830 | Range, mild upside |

| USD/CNY | 6.7570 | Yuan Strength |

Market Lookahead

Wed, 17 Jun

- Eurozone HICP (May)

- Fed Interest Rate decision, FOMC projections

Thurs, 18 Jun

- UK Average Earnings, Claimant count Change, ILO Unemployment rate

- BoE Monetary policy meeting, Interest Rate decision

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.