Energy Prices Force a Rethink at the World's Central Banks

8 min read

Share

Brent Crude tops $103 as the US-Iran war premium builds. The RBA delivered the first rate hike since the conflict began. Seven other central banks face the same dilemma this week. Oil-driven inflation has shifted rate expectations across major currencies. Sterling holds ground, the euro softens, and the dollar extends its lead as the geopolitical safe-haven bid holds firm.

GBP: Resilient but Bruised in an Energy Shock

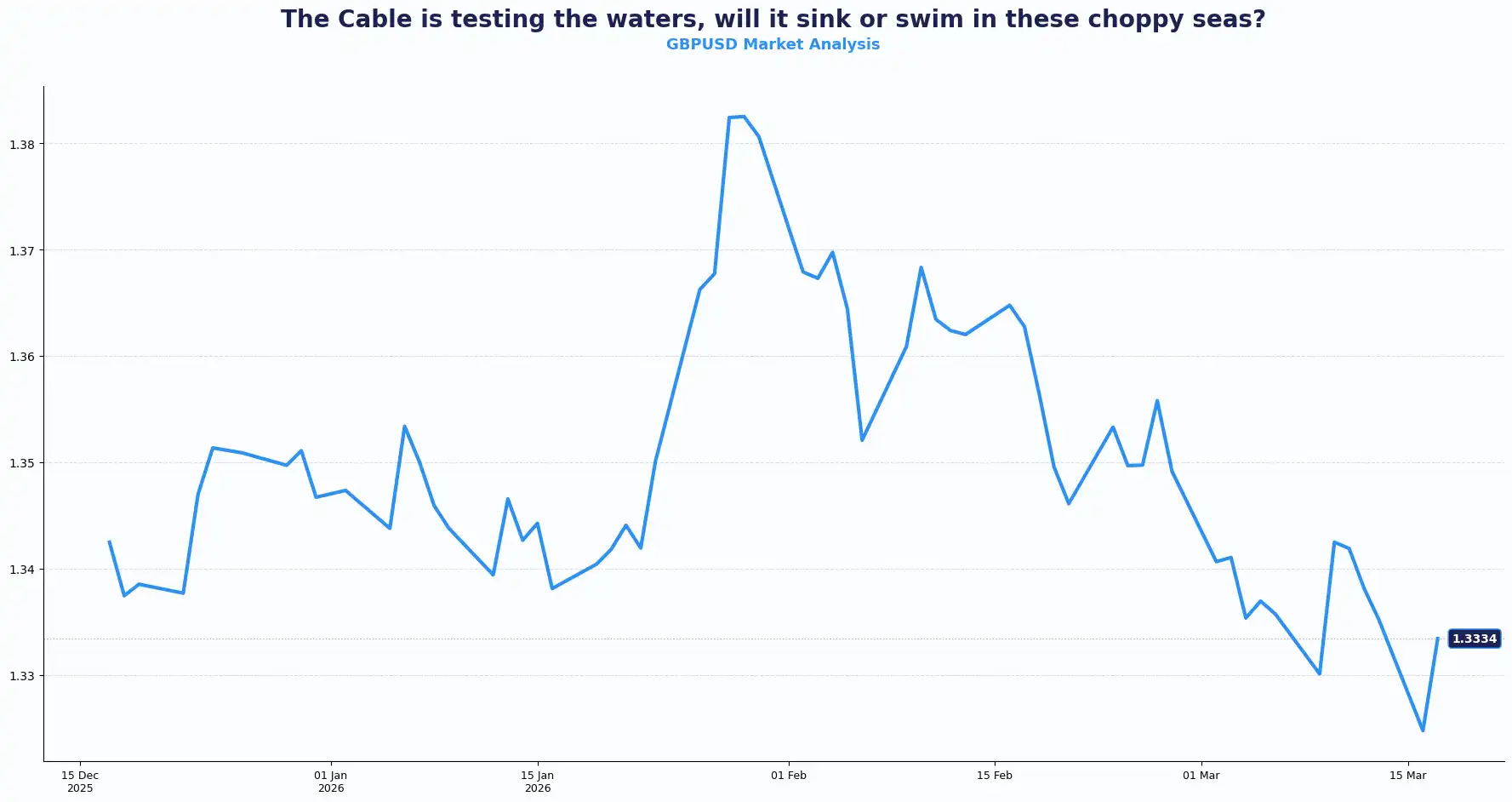

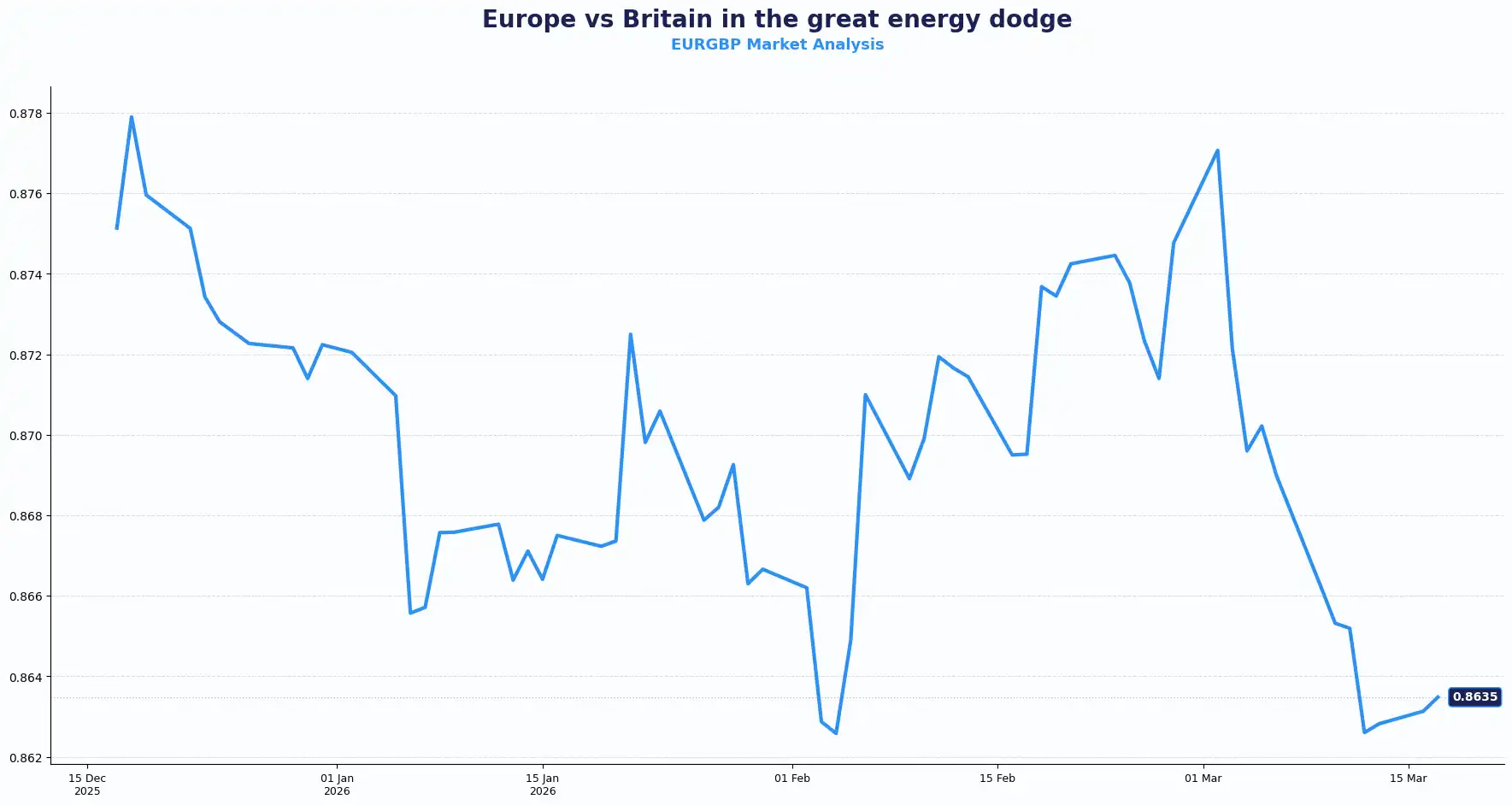

GBPUSD 1.3310 | EURGBP 0.8636

Sterling rebounded above $1.32, pulling back from a three-month low after a 1.7% slide over three weeks. The pound outperformed the yen and the euro, down 2% and 3%, respectively, in the same window. The relative cushion has two drivers: the UK imports less energy than the eurozone or Japan, and UK borrowing rates run higher than both.

Energy prices have forced a hawkish pivot in the Bank of England’s (BoE) rate decision, with the traders now pricing in a 23bps hike for December. The outlook has completely flipped, from early March when two rate cuts were fully priced for the year. A full-quarter point is nearly on the table now.

Thursday’s BoE decision is expected to hold at 3.75%, in line with market consensus. The focus falls on the vote split of the MPC, with a 7-2 or 6-3 decision to hold rates as the most likely base case. A dissenter shifting from rate cut to rate hike would be the hawkish read worth watching.

UK labour data releases on Thursday alongside the BoE rate decision. The claimant count for February is forecast at 24.5k, down from 28.6k previously. The UK ILO unemployment and January employment change data print on the same day. Wage growth, which was once the stickiest part of the UK inflation picture, has started to ease. A softening labour backdrop combined with persistent inflation and rising oil prices puts the BoE in a holding pattern with little flexibility in either direction.

Rate expectations for the BOE moved further and faster than the start-of-month consensus projected. Sterling stability reflects relative strength but not immunity. The pound faces pressure if labour conditions deteriorate further. Shifts in labour data and inflation expectations continue to reshape investor positioning behaviour.

Key technical levels for GBP/USD: Resistance at 1.3350 and Support at 1.3200.

Key technical levels for EUR/GBP: Resistance at 0.8700 and Support at 0.8600.

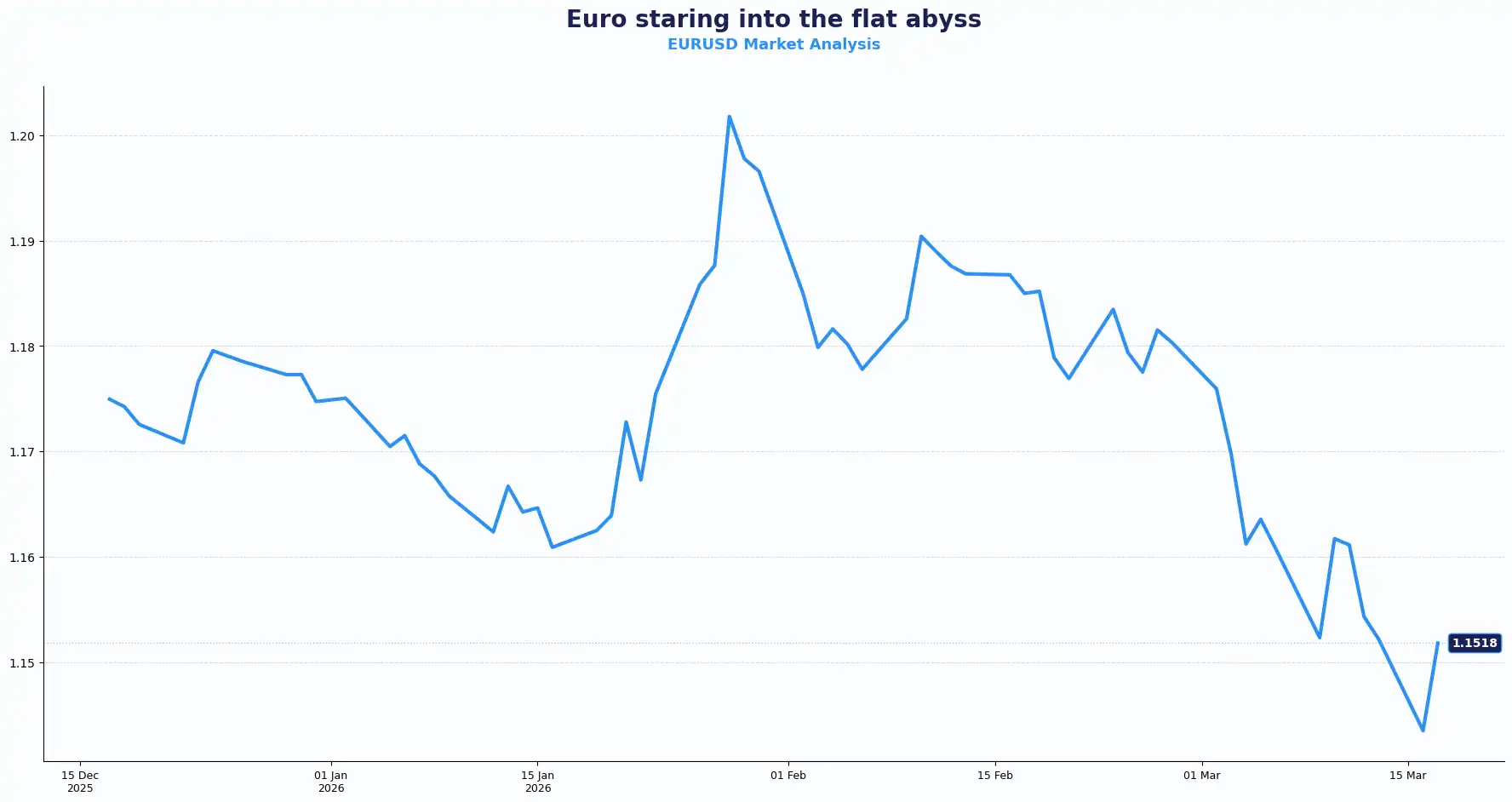

EUR: Eurozone Sentiment Faces Inflation Test

EURUSD 1.1495 | EURGBP 0.8636

The euro sat flat near $1.1499. Against sterling, it held at 86.36 pence. The single currency fell by more than 3% over three weeks. That is the sharpest slide among the major European pairs in that period.

The eurozone's greater reliance on energy imports explains the gap in performance compared with sterling. Germany's ZEW and the Eurozone’s ZEW Economic Sentiment survey data drop today. These are the first institutional investor readings since the escalation of the Middle East conflict. An optimistic outcome could support the euro while a pessimistic one could extend its slide. European Central Bank (ECB) board member Nagel also addresses the public today; his tone on the rate path is likely to draw close attention from investors.

Wednesday (tomorrow) brings the Eurozone HICP figures for February. Headline inflation is forecast at 1.9% YoY and 0.7% MoM, both matching the prior readings. Core HICP is expected to hold at 2.4% YoY, a number that sits near the target on the surface. The oil spike arrived after those forecasts were set, and the upside inflation risk has grown in the gap between then and now.

Thursday, the ECB decides on its deposit facility rate and is expected to hold rates at 2.00%, with the main refinancing rate at 2.15%. The BIS flagged this as a textbook case for “looking through” rather than reacting to a supply shock. The ECB's language on Thursday will signal how far that framing has landed at the Governing Council.

Inflation risk argues against rate cuts, while weak growth argues against hikes. That tension limits the euro upside. The euro reflects policy hesitation. Inflation and growth pull in opposite directions, shaping cautious positioning and muted price action.

The euro's flat reading reflects a balance between structural energy exposure and central bank credibility. HICP on Wednesday and the ECB decision on Thursday test whether current pricing holds or another leg lower begins.

Key technical levels for EUR/USD: Resistance at 1.1550 and Support at 1.1400

USD: Consolidates as the Conflict Premium Holds

DXY 99.89

The dollar index (DXY) gained over 2% this month. Brent Crude hit $103.11 a barrel, up 2.9% on the session. The US-Iran conflict drove a broad repricing of global inflation expectations. The dollar absorbed the resulting flows ahead of gold, the Swiss franc, and government bonds. Geopolitical and rate safe-haven bids stacked on top of each other, and the dollar took them all.

The Fed is due to conclude its two-day meeting on Wednesday. Fed funds futures price a 99.1% probability of no change with rates at 3.75%. FOMC economic projections for the current year and longer are also due on Wednesday. Those projections are expected to carry more weight than the rate call itself.

The Iran conflict continues without resolution as airstrikes persist and supply risks stay elevated. Oil prices respond fast, and inflation expectations follow. The Federal Reserve enters this environment with limited visibility; the FOMC is not expected to signal a firm directional lean. The committee has no way of knowing how long the war will last or which effect will dominate. Geopolitical friction sustains the dollar's strength, and its near-term strength persists while the war risk stays elevated.

President Trump accused Western allies of ingratitude when several countries refused his demand to escort oil tankers through the Strait of Hormuz. Meanwhile, Iran continued targeting Gulf oil infrastructure, and the war premium on oil has no clear exit point yet.

US PPI prints on Wednesday ahead of the FOMC. API crude oil stock data will also be released today, and US Initial jobless claims data will be released on Thursday.

Inflation risk and geopolitical tension continue to shape dollar positioning behaviour across global investors. The picture is likely to change once the war premium in oil fades or the Fed delivers a clearer signal on direction.

Aussie Hikes as Asia-Pacific Falters

AUDUSD 0.7088 | NZDUSD 0.5837 | USDJPY 159.28 | GBPJPY 212.01

The Reserve Bank of Australia (RBA) surprised many with a 25bps hike to 4.10% in a 5-4 vote. Despite the move, the Aussie dollar dropped to test 0.7050 and settled in a 0.7050-0.7100 range.

The vote was tight, yet the logical conclusion was unanimous among all board members, who agreed that inflation was too high. While four members preferred to wait until May, the majority judged that inflation persisting above target for longer outweighed the case for delay. Short-term inflation expectations had already risen before the vote. Bullock put it plainly: the argument was about timing, not direction. A further hike to 4.35% is fully priced by August, and May now carries a 40% probability of an additional move.

The kiwi dropped 0.4% to $0.5843, weighed down by selling pressure against the Aussie. New Zealand Q4 GDP prints on Wednesday and anchors near-term RBNZ expectations.

The yen weakened to $159.31, approaching the 160 level that draws intervention talk. Bank of Japan (BoJ) Governor Kazuo Ueda told reporters that underlying inflation is moving toward the 2% target, ahead of Thursday's BoJ policy decision, which is expected to keep the rate at 0.75%. Some analysts set a higher bar for actual intervention given elevated oil prices. Overall, the yen has fallen by more than 2% against the dollar since the day the conflict broke out.

Gold prices stay steady at $5,022.28. Bitcoin and Ether both slipped. Stock markets struggle for direction as volatility stays elevated across the board, with the Middle East war continuing without signs of a pause as Israel and Iran trade airstrikes. Investors continue to look out for more data and facts amidst the geopolitical noise for a fresh direction.

Current Rate Table:

| Pair | Rate | Short term Trend bias |

|---|---|---|

| GBPUSD | 1.3310 | Bearish Recovery |

| EURUSD | 1.1495 | Rangebound, bearish bias |

| EURGBP | 0.8636 | Stable, Neutral |

| AUDUSD | 0.7088 | Soft, rangebound |

| NZDUSD | 0.5837 | Weak |

| USDJPY | 159.28 | Bullish |

| DXY | 99.89 | Strong |

(*rates as at the time of writing)

Market Lookahead

Tue, 17 Mar

- EUR - Germany ZEW & Eurozone ZEW Economic Sentiment; ECB Nagel speech;

- USD - API Crude Oil Stocks

Wed, 18 Mar

- EUR - Eurozone HICP Final (Feb)

- USD - US PPI; Fed Rate Decision, FOMC Economic Projections

- NZD - New Zealand Q4 GDP

- JPY - Japan foreign investment data

Thu, 19 Mar

- GBP - UK Claimant Count (Feb), ILO Unemployment + Employment Change (Jan);

- GBP - BOE Rate Decision

- EUR - ECB Rate Decision - Deposit facility rate

- USD - US Initial Jobless Claims

- JPY - BoJ Rate decision

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.