Central Bank Divergence and Hanging US-Iran Pact Stir FX

7 min read

Share

US-Iran draft deal and central bank divergence reshape major currency pairs. The dollar steadies, sterling softens, and the yen ticks up after the BOJ hikes rates to 1%. RBA held its rate. Attention now shifts to the BoE and the Fed next, with upcoming inflation data, rate expectations, and a data-heavy week for the UK.

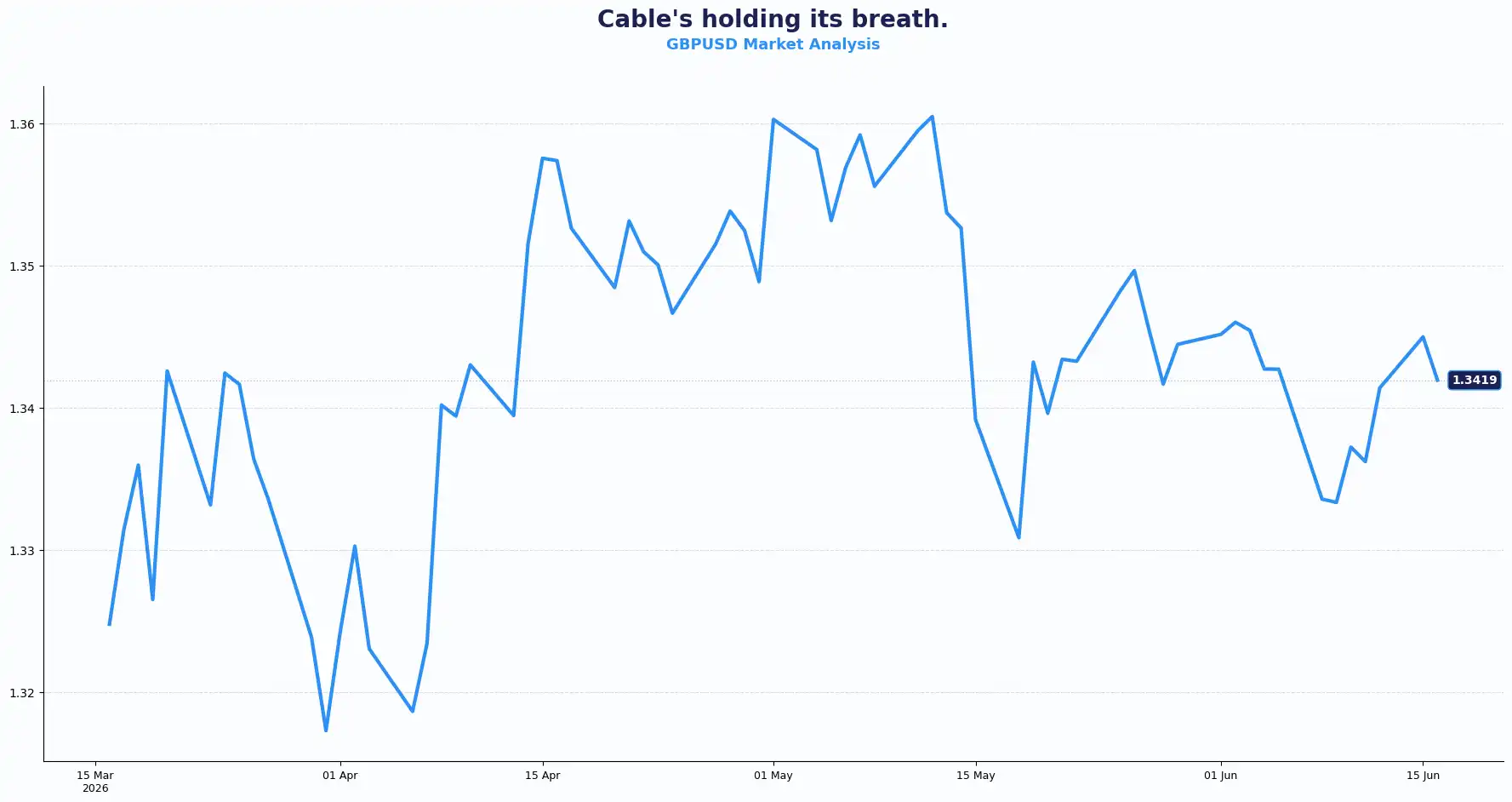

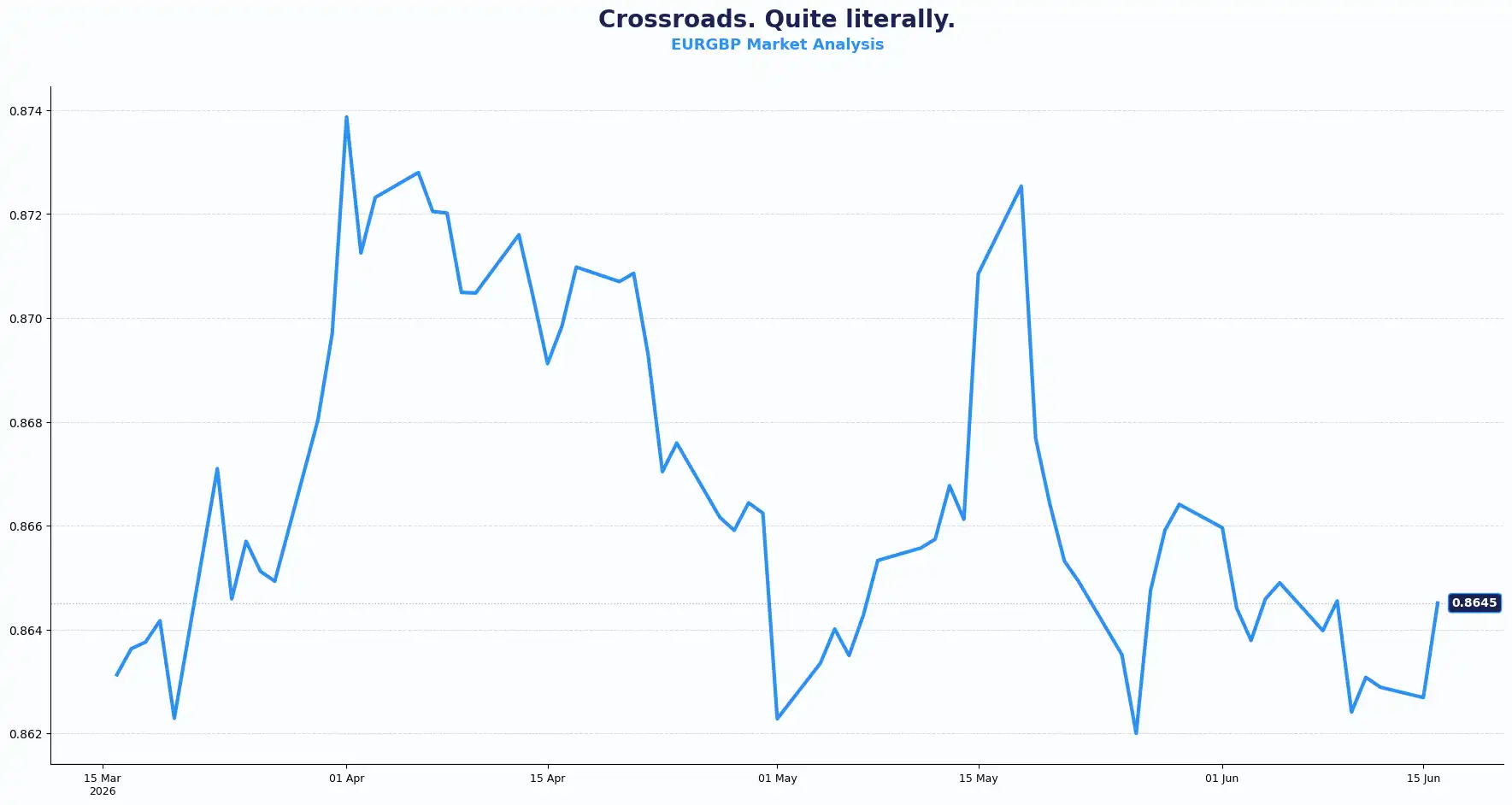

GBP: British Pound Edges Lower Amid US-Iran Peace MOU

GBPUSD 1.3419 | EURGBP 0.8645

Cable slipped towards 1.3400 in the Asian and early European sessions on Tuesday, pulling back after a modest bounce the day prior. The dollar draws support from caution surrounding the US-Iran peace talks, and the pair drifts lower in that risk-off undertow.

The MOU signed electronically between Washington and Tehran has not been accompanied by any official text. Iranian President Masoud Pezeshkian described it as a draft, not a final agreement. Major shipping lines are holding vessels rerouting until full transparency on the Strait of Hormuz situation is established. This hesitation has kept Oil above $83 a barrel and energy price risk alive, a headache for an economy already watching its inflation trajectory.

The UK faces a high-density data week. UK (CPI) inflation figures arrive tomorrow, alongside the Producer Price Index (PPI) and the Retail Price Index data. The UK’s Employment figures and retail sales follow later in the week. The Bank of England (BoE) meets on Thursday and is widely expected to hold the base rate at 3.75%. Thursday also brings the Makerfield by-election, adding a layer of domestic political noise.

For sterling, the combination of a cautious dollar, pending BoE commentary, and live inflation data creates a week when direction will be determined by the data, not by positioning alone. UK CPI expectations and the BoE's post-decision language are the two things investors are watching closely.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3500 and Support sits at 1.3350, 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8680, 0.8720 and Support sits at 0.8600, 0.8560

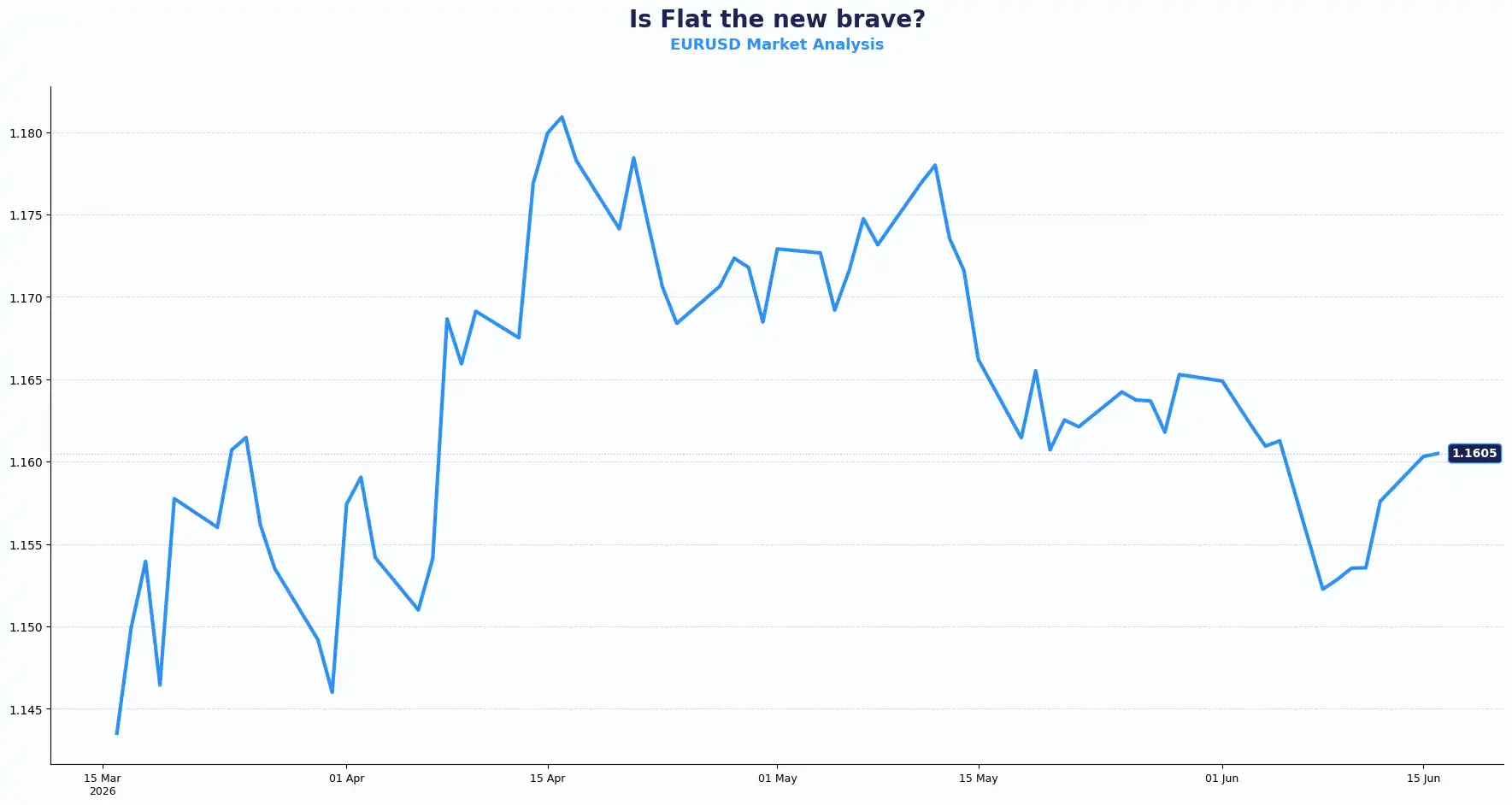

EUR: Euro Confronts Trade Crosswinds

EURUSD 1.1605

European equity indices open mixed on Tuesday. The German DAX adds 1.1%, France's CAC 40 gains 0.4%, but the FTSE 100 drops 0.4% as falling oil prices hit BP and Shell. The pan-European STOXX 600 edges up just 0.2%. The euro holds around 1.1579 against the dollar.

The structural story for the EUR/USD pair goes beyond central bank calendars. Media reports suggest that EU officials have accused China of training Russian troops and are considering sanctions and tariffs in response. A European shift toward the US position on China could carry real trade and growth implications for the euro. The EU also formally launched accession processes for Ukraine and Moldova this week, as Russian attacks on Kyiv escalate. This is geostrategically significant, even if the accession process could run for years.

Tomorrow brings the Eurozone's Core HICP inflation print for May. The Core HICP strips out food, energy, alcohol, and tobacco, giving the clearest read on underlying price pressure. A reading above consensus could reinforce the European Central Bank's (ECB) existing stance. A softer reading could prompt reassessment. Investors will be watching to see whether the data closes or widens the policy gap with the Fed.

The ZEW economic sentiment survey from Germany is due later in today's session, alongside US housing starts and import/export price data.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1640, 1.1700 and Support sits at 1.1520, 1.1480

USD: Dollar Holds as Wall Street Weighs Iran Deal Limits

DXY 99.75

The dollar holds near a ten-day low. Gold trades at $4,326 per ounce, up more than 2% from last week's levels. Brent crude sits just below $83 per barrel after settling at a three-month low overnight. US equities rose on the peace deal headline and falling oil, but the mood on Wall Street is more cautious than the equity move suggests.

The core issue seems to be that no one knows the deal's terms. Trump announced the MOU on Sunday. Formal in-person signing is scheduled for Friday in Switzerland. But the absence of any published text would suggest that energy infrastructure normalisation along the Strait of Hormuz may not be happening yet. Shipping confidence would need rebuilding, potential de-mining operations are another factor, and some economists flag that even a best-case scenario could take months to normalise global energy flows.

The Federal Reserve (Fed) concludes a two-day meeting on Wednesday. Kevin Warsh, in his first meeting as Chair, was widely expected to hold rates at 3.50%-3.75%. His post-meeting press conference is what most investors would be looking at for cues on the Fed’s further direction, potentially impacting dollar moves. Markets’ Fed rate hike expectations for December have eased to 57% probability, down from around 70% last week, according to CME FedWatch. If Warsh signals any openness to cuts later in 2026, the dollar could soften further, and gold would push higher. A more hawkish lean would support the dollar and cap gold's recent run. Warsh's tone on inflation, employment, and the US economic outlook could potentially set the direction for the dollar and dollar pairs for the rest of the week.

Asia-PAC Diverges: BoJ Hikes, RBA Pauses

AUDUSD 0.7053 | NZDUSD 0.5806 | USDJPY 160.27 | GBPJPY 214.73

JPY: The Bank of Japan (BoJ) raised its overnight rate target to 1% today, the highest level since 1995. The vote was 7 to 1, with board member Toichiro Asada dissenting on the grounds that downside output and employment risks outweigh upside inflation risk. Governor Ueda was absent for medical reasons, as previously announced. The BOJ confirmed that accommodative financial conditions will continue after the hike, signalling the tightening path is gradual, not abrupt.

The yen has faced sustained pressure from heavy carry trade positioning. Traders have borrowed in yen to fund higher-yielding assets elsewhere, and the wide gap between Japanese and US interest rates still supports that trade even after the hike. The USD/JPY pair trades near 160.27, reflecting the carry dynamic. The BOJ's hike does address the inflation risks the Iran conflict introduced, but the structural yen weakness from the rate differential is not resolved by a single 25 basis point move.

AUD: The Reserve Bank of Australia (RBA) held the cash rate at 4.35% in a unanimous nine-member board vote. This is the first hold after three consecutive hikes this year from a starting point of 3.60%. The RBA noted that inflation is still too high and that higher energy costs pose upside risks. But recent softer economic data created enough room to pause and assess the impact of prior tightening.

Governor Michele Bullock's press conference is due later today. The key question is whether the RBA signals an extended pause or retains an explicit tightening bias. About 30% of money market pricing points to a further hike at the August meeting. Around 60% price in one final hike to a peak rate of 4.60%. The AUD/USD pair trades at 0.7053, off 0.3% on the day and retreating from Monday's bounce, which had lifted the pair almost 0.5% on initial Iran deal optimism.

NZD: The NZD/USD pair sits at 0.5806, also down 0.3% on the day. The pair met resistance at 0.5865 overnight and now finds support at last week's low of 0.5770. The kiwi's direction this week follows broader risk sentiment and the RBA's signals rather than domestic data.

Broader Asia FX: Oil above $80 per barrel, even on peace deal optimism, creates inflation-linked pressure across Asian currencies. Indonesia, the Philippines, and India face the most acute exposure due to deteriorating trade balances and slowing foreign direct investment. Any further normalisation in Persian Gulf crude flows could give IDR, PHP, and INR room to recover ground, but the timeline for that normalisation is unclear. Asian central banks with import-heavy economies are watching the Fed closely; a hawkish Warsh could intensify rate-hike pressure in the region.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3419 | Sideways |

| EUR/USD | 1.1605 | Sideways |

| EUR/GBP | 0.8645 | Sideways |

| USD/JPY | 160.27 | Sideways/Bearish |

| GBP/JPY | 214.73 | Sideways |

| AUD/USD | 0.7053 | Bearish |

| NZD/USD | 0.5806 | Bearish |

| DXY | 99.75 | Bearish |

Market Lookahead

Tues, 16 Jun

- Germany & Eurozone ZEW Economic Sentiment (June)

Wed, 17 Jun

- UK CPI (May)

- UK PPI (May)

- UK Retail Price Index (May)

- Eurozone HICP (May)

- Fed Interest Rate decision, FOMC projections

Thurs, 18 Jun

- UK Average Earnings, Claimant count Change, ILO Unemployment rate

- BoE Monetary policy meeting, Interest Rate decision

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.