A Crude State of Affairs Across the Crosses

7 min read

Share

Brent up 58% in March, Gulf tensions continue to influence rate paths, a hawkish reprice and a dollar that barely flinched. Sterling and the euro absorbed the cost. Eurozone CPI looming. Central banks face a stagflation bind as geopolitics redraws rate expectations.

GBP: Sterling Slides as Risk Appetite Dries Up

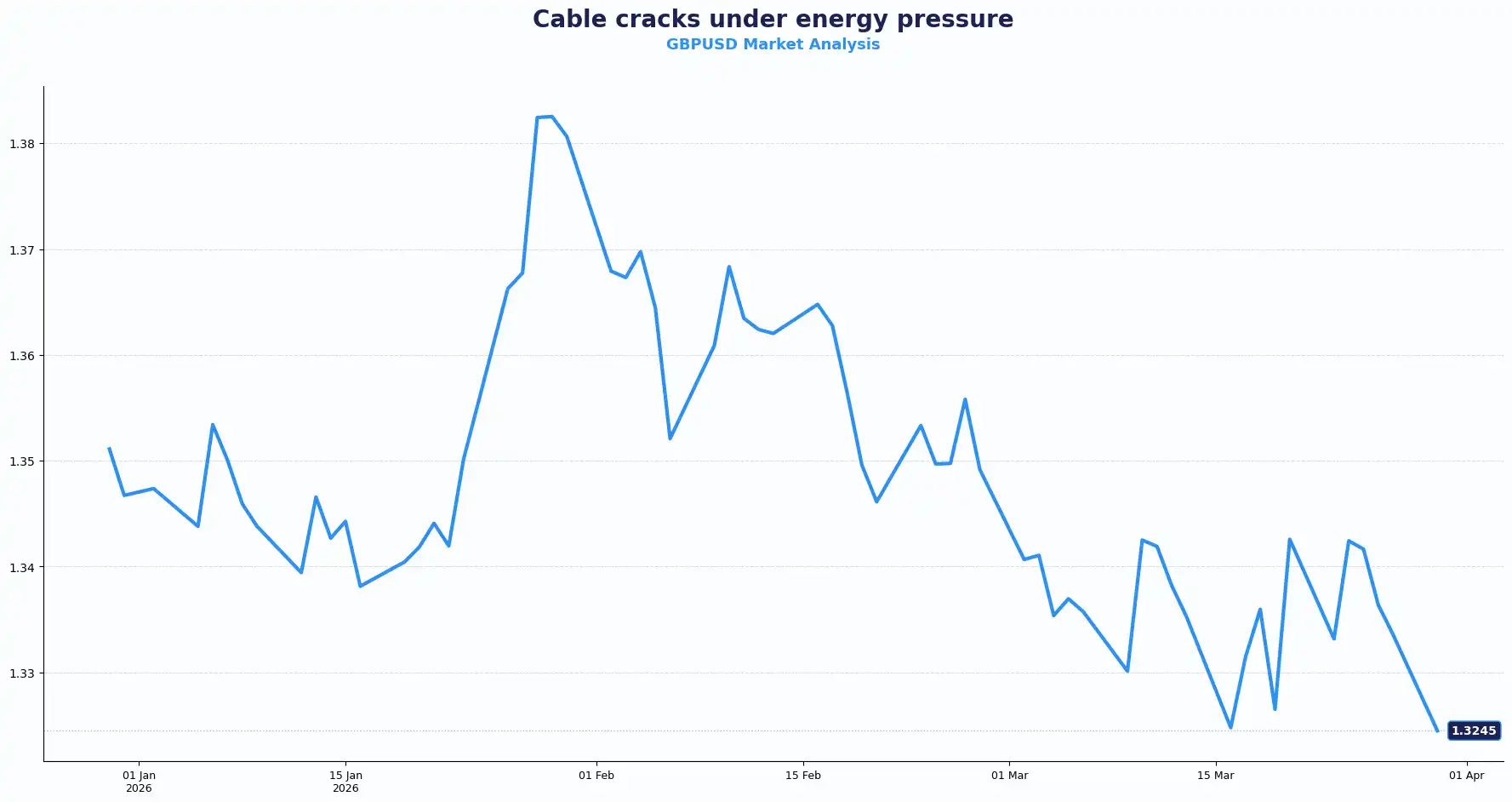

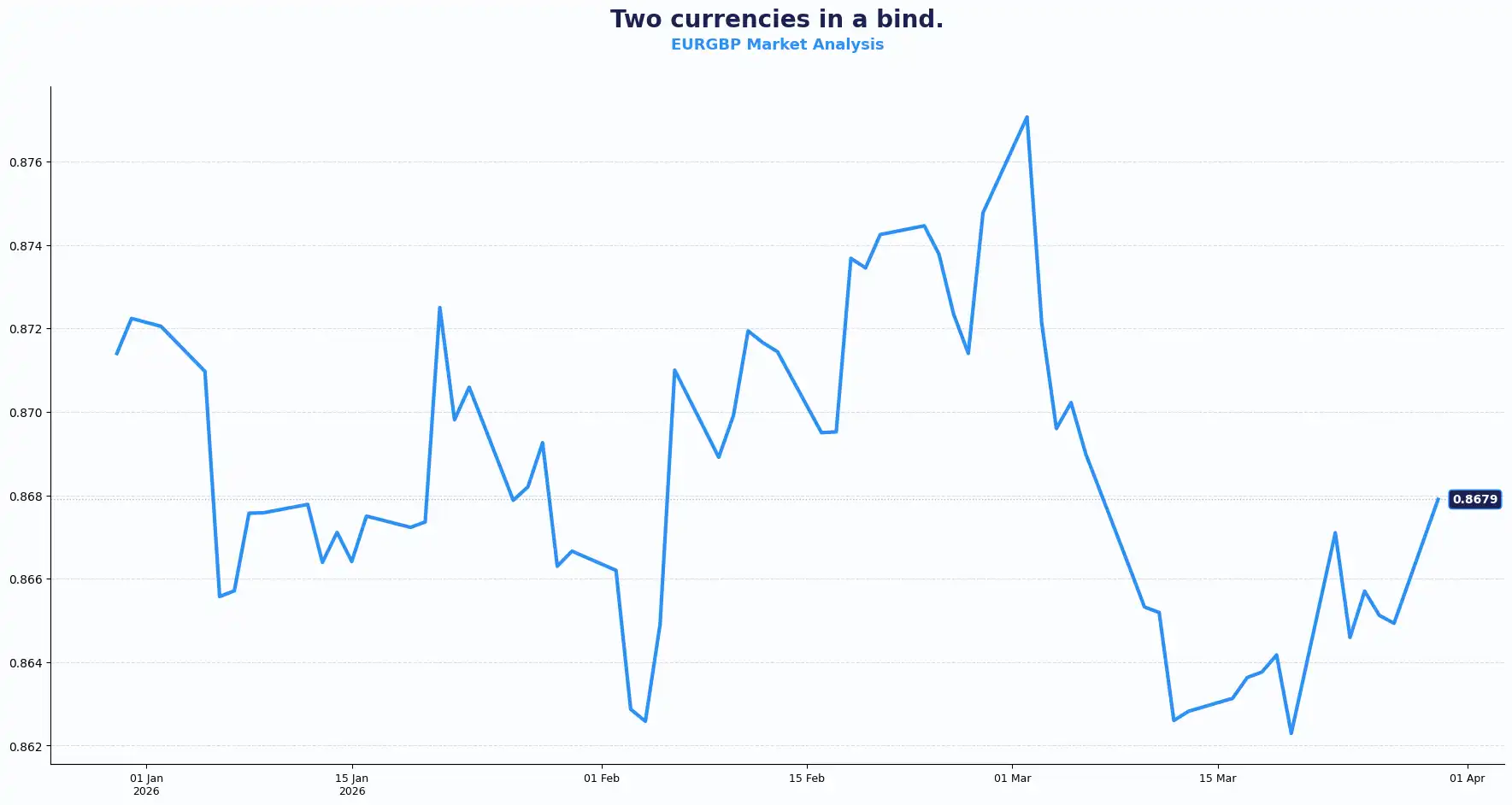

GBPUSD: 1.3240 | EURGBP: 0.8677

Sterling opened the week under intense pressure. GBPUSD trades near 1.3240, the lowest point in a fortnight, and is on track for a 1.7% monthly decline. As the conflict in the Middle East widens with Yemen’s Houthis launching strikes on Israel and fears of broader regional escalations mounting, investors are seen fleeing riskier assets.

This fragile situation amplifies the "stagflation calling card," hitting the UK particularly hard. Supply chain disruptions through the Red Sea threaten to bake higher costs into the British economy just as growth signals turn cautious. The war, ignited by strikes on Iran on 28 February, now spans the region and if Houthis restrict this passage, the energy trade faces a double stranglehold.

The macro picture adds nothing to support Sterling's case. UK Q4 GDP data drops tomorrow. The Consensus is 0.1% QoQ and 1.0% YoY, identical to the prior reading. Flat growth. Flat expectations. No catalyst. Any deviation will likely exacerbate the pound's vulnerability.

Energy costs will filter through UK CPI prints in the weeks ahead. Rate derivative pricing has already moved, and earlier bets on aggressive Bank of England (BoE) easing have been scaled back. The BoE now confronts the stagflationary bind that every central bank faces right now: tighten into a slowdown, or ease and let inflation take hold, and truly neither path is going to be comfortable.

Meanwhile, EUR/GBP held near 0.8677. With eurozone CPI due Tuesday and ECB hawks getting louder, euro strength relative to sterling is a live theme this week. Elevated energy price volatility of this kind has, in past cycles, been associated with a repricing of UK rate expectations and wider shifts in GBP positioning.

Current volatility has fundamentally shifted the cost of inaction. Any deviation will shape near-term sterling direction, though oil still sets the broader tone for now.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3350, 1.3420 and Support sits at 1.3200, 1.3150

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8720 and Support sits at 0.8620

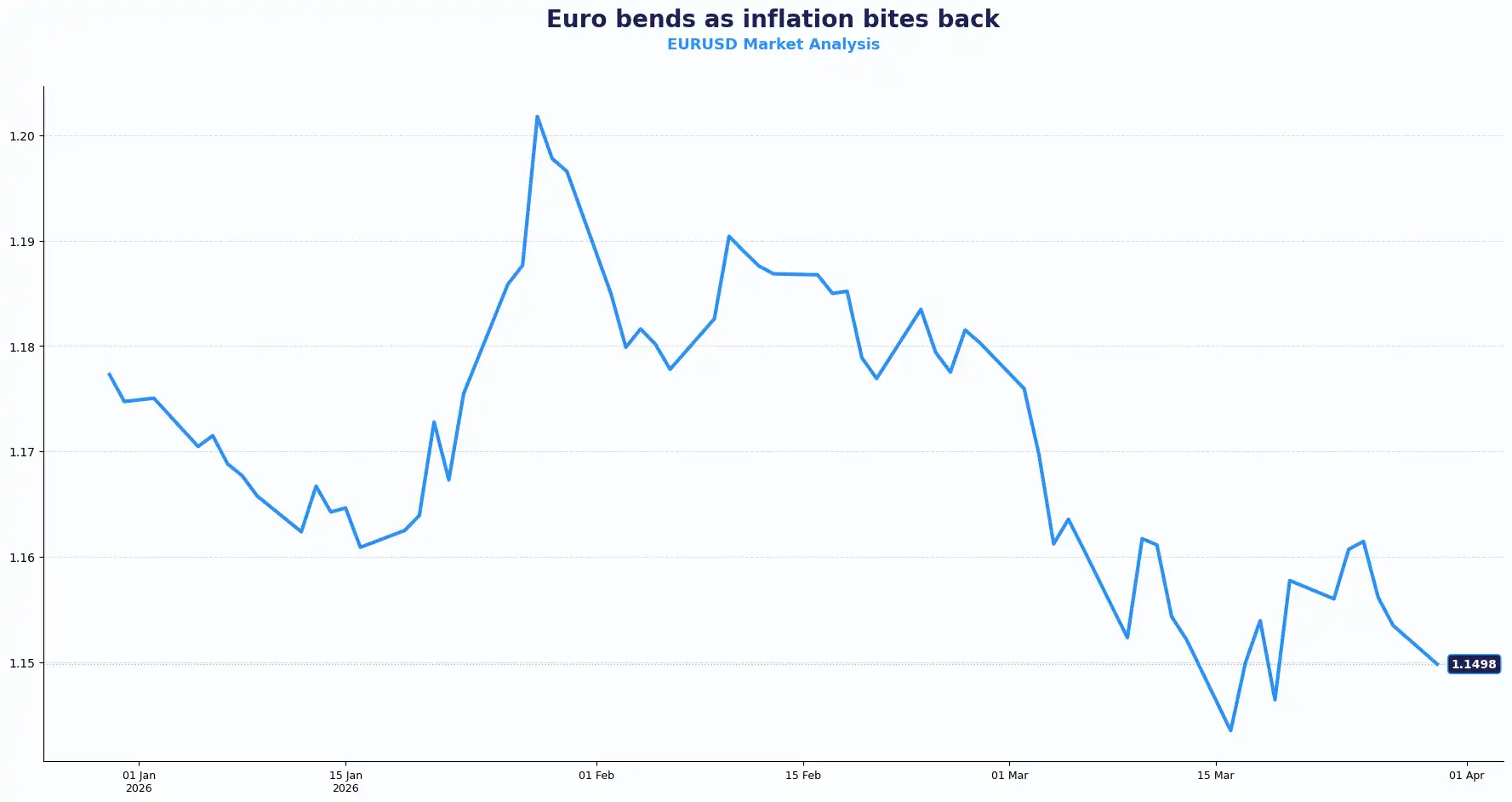

EUR: Eurozone Braces for an Inflationary Storm

EURUSD: 1.1514

EURUSD trades near 1.1514, with the euro staring down a 2.5% loss for March. Europe's energy dependency makes this oil shock cut deeper here than across the Atlantic.

This energy shock is reshaping the European Central Bank (ECB)'s strategy. Higher oil and gas prices could push headline inflation above 3% in 2026 before easing to the 2% target in 2027, while core inflation is likely to re-accelerate as energy costs feed through supply chains.

The bank faces the same bind playing out across the G7, forcing a choice between supporting a fragile economy or aggressive rate hikes to kill the inflationary beast. The ECB hawks are urging hikes and rate derivative pricing implies a 58% probability of an April rate hike.

Germany's March CPI is due today (forecast: 0.9% MoM, prior: 0.2%). The eurozone CPI, out Tuesday, is expected at 2.7% YoY, up from 1.9% in February. Core prices should stay steadier, but the trend is clear.

A strong CPI print on Tuesday has, in past cycles, been associated with upward pressure on EUR rate futures and a pickup in EUR/USD volatility. However, current volatility benefits the dollar as the world's most liquid asset. Today's calendar also includes the eurozone IFO Business Climate and Consumer Confidence for March. German import price index and retail sales for February follow on Tuesday. Traders have been treating this week's data pack as a pivotal input.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1600, 1.1680 and Support sits at 1.1450, 1.1380

USD: Dollar Continues to Dominate the Global Arena

DXY: 100.10 | BRN CRUDE $114.60

The dollar Index (DXY) trades near 100.10 and heads for its strongest monthly gain since July. The dollar holds firm as oil drives inflation risk, and risk sentiment turns cautious.

Brent Crude touched $114.60 earlier in the session before settling near $108.00 at the time of writing, up about 58% in March. That puts it on course for the biggest monthly rise on record, surpassing even the surge triggered by Iraq's invasion of Kuwait in 1990.

The US benefits from its status as an energy exporter, which buffers the inflation shock relative to Europe and Asia. At the same time, higher oil prices revive inflation concerns and shift rate expectations.

Meanwhile, Trump stated Washington held both direct and indirect talks with Iran, describing the new Iranian leadership as "very reasonable." In the same session, he floated the idea of seizing Kharg Island, Iran's main oil export terminal. Two readings of the same situation emerged: while some investors largely ignored the White House's comments on "reasonable" Iranian leadership, others drew their own conclusions amid the uncertainties.

The "Fed pivot" has evaporated. Markets have given up bets on 2026 rate cuts, now pricing in the risk of a Fed hike later this year. The dollar’s status as a net energy exporter gives the US a massive structural advantage over Europe and Asia, which are currently dependent on Middle Eastern energy flows.

Where oil goes, the dollar follows. The rapid shift in probabilities from "low-risk" to "US boots on the ground" scenarios has altered the playbook for the global FX landscape.

Looking ahead, data on retail sales, manufacturing, and payrolls will update the economic outlook this week. JOLTS job openings (February) and Consumer Confidence (March) data release tomorrow (Tuesday). Non-farm payrolls for March are forecast at +55,000 after February's surprise drop of 92,000. Unemployment is expected to hold at 4.4%. The dollar thrives on this uncertainty. The dollar rate premium has repriced at speed this month. That kind of shift has, in past cycles, been associated with reassessments of cross-currency basis and USD carry dynamics.

Yen and Antipodeans Strain Under Energy Shock

AUDUSD: 0.6868 | NZDUSD: 0.5736 | USDJPY: 159.76 | GBPJPY: 212.01

The yen has plummeted past the 160 level, its weakest since July 2024. Despite Governor Ueda’s "jawboning" and threats of "decisive steps" from currency diplomat Atsushi Mimura, the yen has dropped 2% in March. Meanwhile, the Aussie and Kiwi dollars struggle as global growth fears outweigh domestic rate-hike expectations.

Asia’s heavy reliance on Middle Eastern energy makes it the primary victim of a closure of the Strait of Hormuz. The drawdown in buffer supplies sparks dramatic price increases across everything from fertiliser to pharmaceuticals. Japan’s reversal signals that fundamentals, not speculation, now drive the yen’s decline.

The prolonged closure of trade chokepoints creates a structural drain on energy-importing economies. Oil-driven stagflation concerns of this type have, in past cycles, been associated with shifts in positioning across risk-sensitive currencies and commodity-linked FX pairs.

Current Rate Table:

| Pair | Level | Short-term Trend |

|---|---|---|

| GBPUSD | 1.3240 | Bearish bias |

| EURUSD | 1.1514 | Bearish bias |

| EURGBP | 0.8677 | Range to bid |

| USDJPY | 159.76 | Bullish USD |

| AUDUSD | 0.6868 | Bearish bias |

| NZDUSD | 0.5736 | Bearish bias |

| GBPJPY | 212.01 | Bullish bias |

(as at the time of writing)

Market Lookahead

Mon, 30 Mar

- German preliminary CPI

- EU economic confidence

- Fed speeches

- G7 virtual meeting

Tues, 31 Mar

- UK Q4 GDP

- Germany import prices and retail sales

- Eurozone CPI

- US JOLTS job openings & US consumer confidence

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.